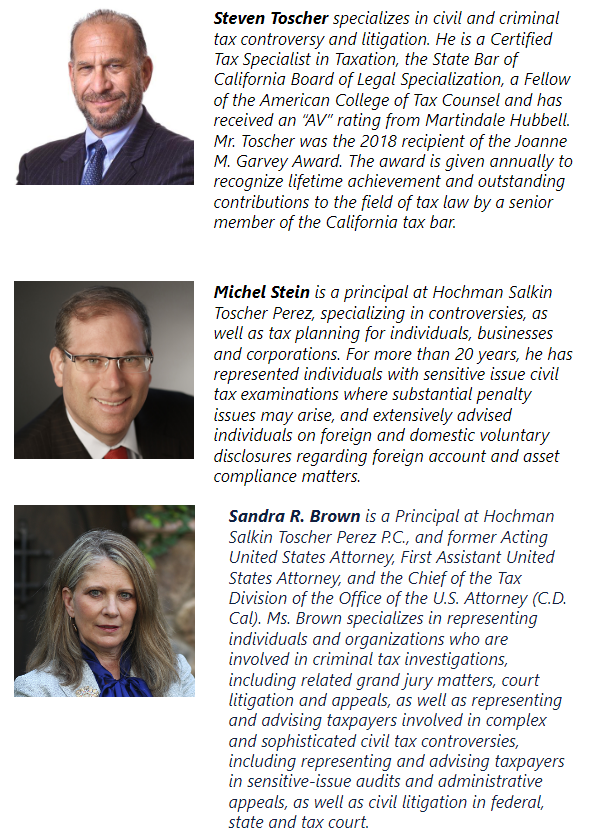

We are very pleased to announce that Sandra R. Brown has been appointed vice chair of the Section’s Civil and Criminal Tax Penalties Committee for the 2023-2024 term. Sandra’s selection as a committee vice chair and as a Section leader represents recognition by her peers of her abilities and contributions to the work of the Section.

Sandra has over 30 years of experience as a tax attorney specializing in the representation of clients in civil and criminal tax cases, including civil audits and appeals, tax collection matters, criminal investigations, and in civil and criminal trials and appeals in federal courts. Prior to joining Hochman Salkin Toscher Perez, P.C., in 2018 as a principal, Sandra was the Acting United States Attorney, the First Assistant United States Attorney, and the Chief of the Tax Division for the United States Attorney’s Office, Central District of California.

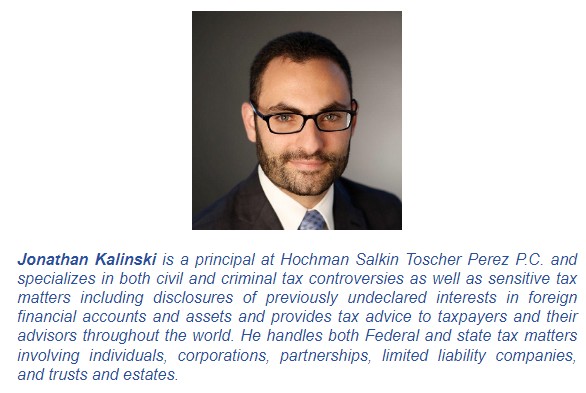

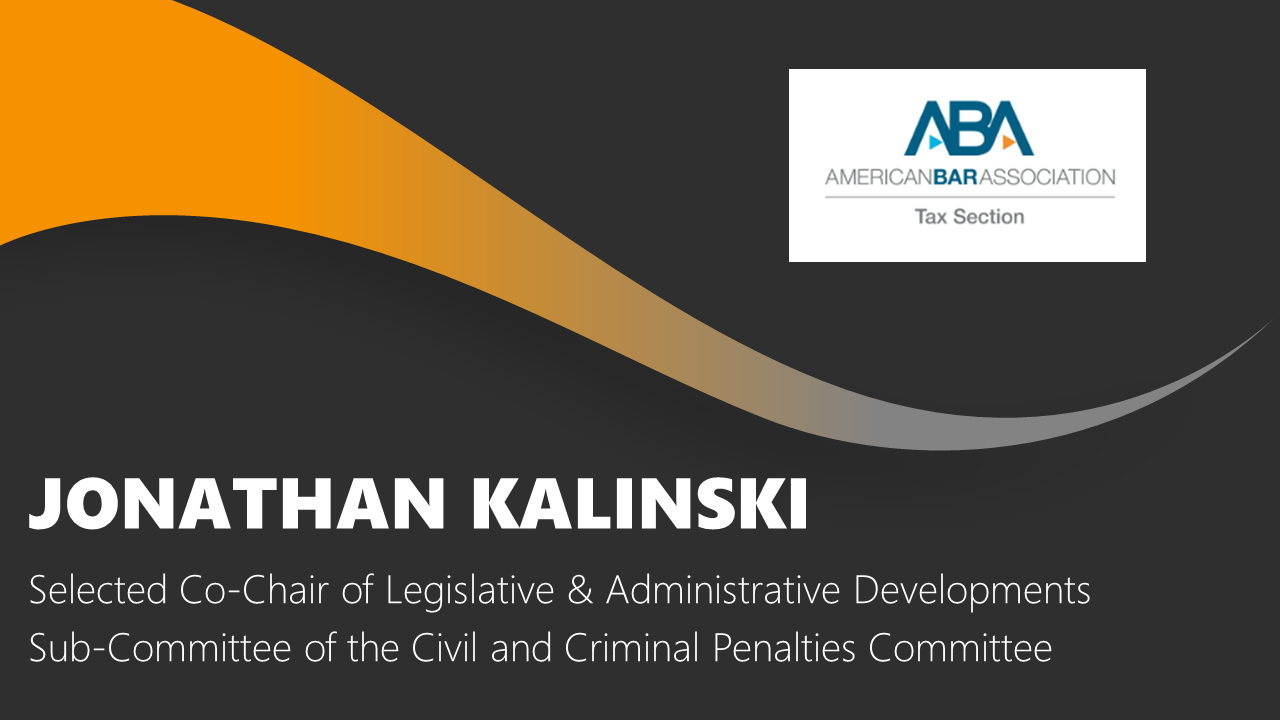

We are also pleased to announce that Jonathan Kalinski has been selected as co-chair of the Legislative & Administrative Developments Sub-Committee of the Civil and Criminal Penalties Committee for the 2023-2024 term.

Jonathan specializes in both civil and criminal tax controversies as well as sensitive tax matters including disclosures of previously undeclared interests in foreign financial accounts and assets and provides tax advice to taxpayers and their advisors throughout the world. Jonathan has considerable experience handling complex civil tax examinations, administrative appeals, and tax collection matters. Prior to joining the firm, he served as a trial attorney with the IRS Office of Chief Counsel litigating Tax Court cases and advising Revenue Agents and Revenue Officers on a variety of complex tax matters. Jonathan Kalinski also previously served as an Attorney-Adviser to the Honorable Juan F. Vasquez of the United States Tax Court.