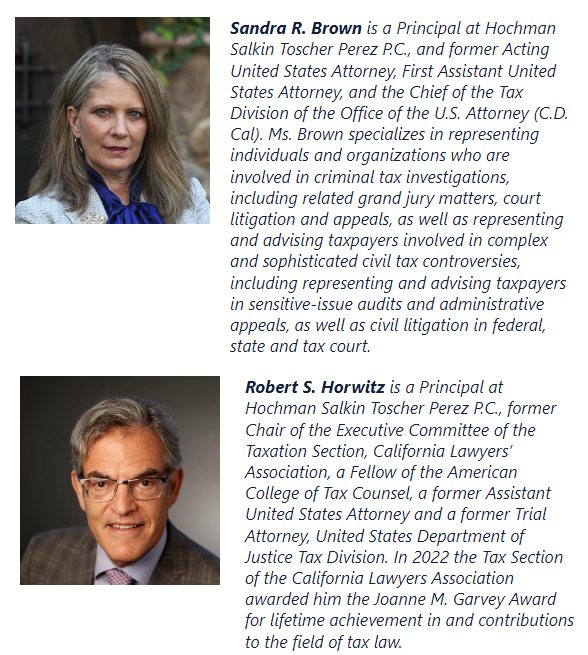

We are pleased to announce that Steven Toscher, Michel R. Stein, and Philipp Behrendt will be speaking at the upcoming Strafford webinar “Tax Treatment of Crypto Staking Rewards: Revenue Ruling 2023-14, Tax Filing Requirements, Managing IRS Examinations,” Tuesday, November 20, 2023, 10:00 a.m. – 11:30 a.m. (PST).

Cryptocurrency has exploded over the last few years causing significant concerns regarding the taxation of these transactions for sellers, purchasers, and investors. Tax counsel and accountants for clients holding and selling cryptocurrency and those engaging in transactions involving crypto staking rewards must understand applicable tax rules, reporting requirements for these transactions, and the tax treatment of crypto staking rewards.

Crypto staking is when a person pledges their cryptocurrency to help validate transactions on the blockchain. This allows crypto holders an opportunity to put their digital assets to work and earn passive income without selling them. However, such transactions are now subject to certain tax treatment for those engaging in these transactions.

Recently, the IRS issued Revenue Ruling 2023-14, guidance directly addressing the tax treatment of crypto staking rewards. The new guidance generally provides that rewards received in exchange for cryptocurrency staking are included in a taxpayer’s gross income in the taxable year in which the taxpayer first has the ability to dispose of the cryptocurrency received. In addition, this may require amending prior year tax returns for taxpayers who failed to report such staking rewards and those who previously reported such staked assets as income if the taxpayer did not have such dominion or control.

Tax counsel and advisers must recognize applicable tax rules for crypto staking rewards and define proper reporting and tax treatment for these transactions.

Listen as our panel discusses critical tax considerations for crypto staking rewards, Revenue Ruling 2023-14, analyzing IRS monitoring to increase compliance, and defining proper reporting and tax treatment for crypto staking rewards.

We are also pleased to announce that we will be able to offer a limited number of complimentary and reduced cost tickets for this program on a first come first serve basis. If you are interested in attending please contact Sharon Tanaka at sht@taxlitigator.com.

Click Here for More Information