On July 3, 2025, the House of Representatives narrowly passed the Republicans’ sweeping reconciliation package, the One Big Beautiful Bill, by a 218-214 vote, which President Trump signed on July 4. The legislation marks the most extensive tax package since the 2017 Tax Cuts and Jobs Act (TCJA), making many of the TCJA’s temporary provisions permanent and introducing a new set of incentives and enforcement priorities.

The IRS has the power to administratively collect an assessed tax liability through filing a notice of federal tax lien and through levying on a taxpayer’s property. Because the exercise of this power can have serious consequences for a taxpayer, Congress in Internal Revenue Code (“IRC”) §6330 gave taxpayers the opportunity to request a hearing before the Independent Office of Appeals before a levy is made. During such a “collection due process” (“CDP”) hearing, the taxpayer may raise any relevant issue to the unpaid tax or the proposed levy, including a challenge to the existence or amount of the underlying liability if the taxpayer did not previously have an opportunity to dispute the liability. After the hearing, the appeals officer is required to make a determination. In doing so, the appeals officer is required to consider various factors, including any issue raised by the taxpayer. Within thirty days of the determination, the taxpayer can petition the Tax Court for review of the determination. A decision of the Tax Court in a CDP case is reviewable by a federal appeals court.

17th Annual NYU Tax Controversy Forum to be held June 26 and 27 Westin New York, Times Square

You do not want to miss this program.

Two of our principals will be speaking on the following topics:

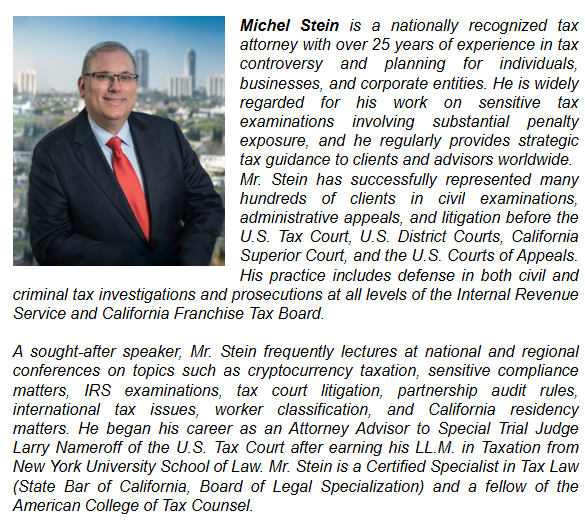

Michel R. Stein Challenging Civil Penalties – Recent Developments June 26

Jonathan Kalinski Who Pays? Third-Party Responsibility in Tax Collection June 27

For 17 years, the NYU School of Professional Studies Tax Controversy Forum has brought together government representatives and expert private practitioners to share their perspectives on a variety of topics involving federal tax audits, appeals, and litigation. The forum covers a wide range of controversy work, from procedural seminars to substantive programs, international issues, ethical problems, current enforcement initiatives, sensitive audits, and civil and criminal tax penalties.

Once again, HOCHMAN SALKIN TOSCHER PEREZ P.C., along with StevenToscher and Sandra R. Brown, have been recognized by Chambers and Partners, 2025 USA, for strength and expertise in the areas of Tax Fraud and Tax Controversy.

Chambers notes HOCHMAN SALKIN TOSCHER PEREZ P.C. is “a respected tax boutique noted for its handling of contentious tax matters. It has a hugely impressive track record in tax controversy, alongside criminal and civil litigation at both state and federal level and is a respected Beverly Hills tax boutique with recognized controversy expertise at both state and federal level.”

Steven Toscheris recognized as “a well-regarded tax practitioner who advises clients on sensitive issues, including criminal tax fraud investigations.” Sandra R. Brown “maintains a highly respected practice concentrated on the representation of clients in criminal tax investigations and civil tax controversies.”

We are also pleased to announce that Chambers High Net Worth – noting our firm’s “bench offers deep governmental experience and additional strength in criminal tax disputes – has also rankedSteven Toscher, Dennis PerezandSandra R. Brown in the area of Tax: Private Client.

Chambers is the world’s leading legal rankings and insights intelligence company. For over 30 years, Chambers has differentiated the very best legal talent by identifying and ranking law firm departments and lawyers globally.

We are honored by the recognition awarded by Chambers and grateful to our clients who continue to trust us with their criminal and civil tax matters. These outstanding achievements are a true testament to the dedication and hard work of the entire team of tax professionals at HOCHMAN SALKIN TOSCHER PEREZ P.C. Our firm looks forward to continuing to provide best in class service to our clients.

Steven Toscher

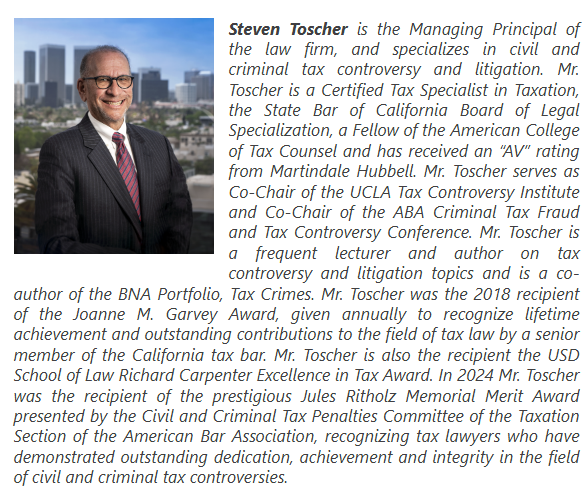

Steven Toscher is the Managing Principal of the law firm, and specializes in civil and criminal tax controversy and litigation. Mr. Toscher is a Certified Tax Specialist in Taxation, the State Bar of California Board of Legal Specialization, a Fellow of the American College of Tax Counsel and has received an “AV” rating from Martindale Hubbell. Mr. Toscher serves as Co-Chair of the UCLA Tax Controversy Institute and Co-Chair of the ABA Criminal Tax Fraud and Tax Controversy Conference. Mr. Toscher is a frequent lecturer and author on tax controversy and litigation topics and is a co-authorof the BNA Portfolio, Tax Crimes.Mr. Toscher was the 2018 recipient of the Joanne M. Garvey Award, given annually to recognize lifetime achievement and outstanding contributions to the field of tax law by a senior member of the California tax bar. Mr. Toscher is also the recipient the USD School of Law Richard Carpenter Excellence in Tax Award. In 2024 Mr. Toscher was the recipient of the prestigious Jules Ritholz Memorial Merit Award presented by the Civil and Criminal Tax Penalties Committee of the Taxation Section of the American Bar Association, recognizing tax lawyers who have demonstrated outstanding dedication, achievement and integrity in the field of civil and criminal tax controversies. For more information, please contact Steven Toscher at toscher@taxlitigator.com.

Dennis Perez

Dennis Perez was formerly a senior trial attorney with District Counsel, Internal Revenue Service, in Los Angeles, California. Mr. Perez is a Certified Tax Specialist, California State Bar Board of Certification and is also a Fellow of the American College of Tax Counsel. He frequently lectures on advanced civil and criminal tax topics at seminars and before national, state and local bar associations and accountancy groups. Mr. Perez is a co-author of the BNA Portfolio, Tax Crimes, served as the Chair of the Los Angeles Lawyer Magazine Editorial Board and is the first recipient of the Los Angeles Lawyer Sam Lipsman Service Award for outstanding service to the Los Angeles Lawyer Magazine. He is past Chair of the Tax Procedure and Litigation Committees of the Taxation Sections of the State Bar of California and the Los Angeles County Bar Association. Mr. Perez is past President of the Alumni Board for the UCLA School of Law and has served as an Adjunct Professor, Golden Gate University, Graduate School of Taxation. For more information, please contact Dennis Perez at perez@taxlitigator.com

Sandra R. Brown

Sandra R. Brown specializes in criminal tax investigations, grand jury matters, litigation and appeals, as well as representing and advising taxpayers involved in complex and sophisticated civil tax controversies, including sensitive-issue audits and administrative appeals, as well as civil litigation. Prior to joining the firm, Ms. Brown served as the Acting United States Attorney, First Assistant United States Attorney; and Chief of the Tax Division in the Office of the U.S. Attorney, Central District of California. During her 27 years as a trial lawyer, she personally handled over 2,000 tax cases on behalf of the United States, including nationally significant civil tax cases such as two Supreme Court decisions and a multitude of published 9th Circuit decisions, as well as a broad range of equally noteworthy criminal tax cases. Ms. Brown obtained her LL.M. in Taxation from the University of Denver, is a fellow of the American College of Tax Counsel, Vice-Chair of the ABA’s Section of Taxation’s Criminal and Civil Tax Penalties Committee, Co-Chair of the UCLA Tax Controversy Institute, Co-Chair of the ABA Criminal Tax Fraud and Tax Controversy Conference, an ABA Loretta Collins Argrett Fellowship Mentor, and is a frequent lecturer and author on tax controversy topics, including international compliance matters. Ms. Brown has been recognized as one of California’s top 100 leading women lawyers and most recently, the recipient of USD School of Law’s Richard Carpenter Excellence in Tax Award and honored at the California Lawyers Association Tax Bar and Tax Policy 2024 Toast to Women in Tax. For more information, please contact Sandra Brown at brown@taxlitigator.com.

In a coordinated move that should command the attention of financial institutions, fintech startups, crypto platforms, and tax professionals alike, on June 10, 2025, the Joint Chiefs of Global Tax Enforcement (J5) released a trilogy of threat assessments aimed at exposing how emerging technologies are facilitating global financial crimes, including tax evasion. These reports, developed through the J5’s Global Financial Institutions Partnership (GFIP), provide a sobering view of how financial technology (fintech), identity-based fraud, and trade-based money laundering are increasingly undermining tax enforcement efforts. Of particular interest to taxpayers, financial professionals, and digital asset platforms is the report titled Misuse of Fintech to Enable Tax Evasion and Money Laundering (dated May 2025), which synthesizes both empirical observations and literature reviews to show how fintech is being exploited to move untaxed income across borders, anonymize financial flows, and bypass regulatory safeguards.

We are pleased to announce thatMichel R. Stein, Robert S. Horwitz and Melissa Briggs will be speaking at the upcoming Strafford webinar, International Tax Disputes, FBAR Violations, Form 3520, Excessive Fines, Friday, June 20, 2025, 10:00 a.m. – 11:50 a.m. (PST).

This webinar will analyze the most recent and relevant court cases affecting international taxpayers. Our panel of foreign tax veterans will detail the status of recent and notable cases and offer insights for handling common international tax and compliance problems. International tax practitioners and advisers need to stay abreast of the continually increasing number of cases and matters brought against multinational taxpayers by the U.S. government.

We are pleased to announce thatRobert S. Horwitz along with Jenni Black (Citrin Cooperman) will be speaking at the upcoming Beverly Hills Bar Association webinar, BBA Audits: What Tax Attorneys Need to Know webinar, Tuesday, June 3, 2025, 12:30 p.m. – 1:30 p.m. (PST).

The webinar will provide an in-depth look at how the Bipartisan Budget Act (BBA) has transformed partnership audits, including the centralized partnership audit procedures under IRC §§ 6221–6241. The panel will guide attendees through the key components of a BBA audit—from the designation and powers of the Partnership Representative, to the calculation and modification of imputed underpayments, to the decision-making process between paying at the partnership level versus electing a push-out.

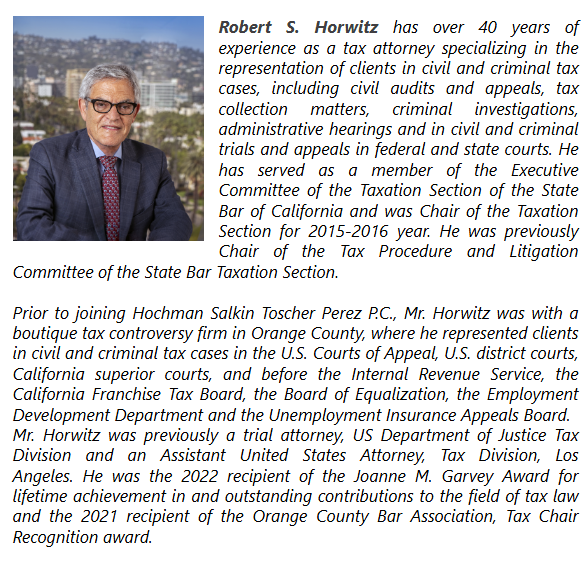

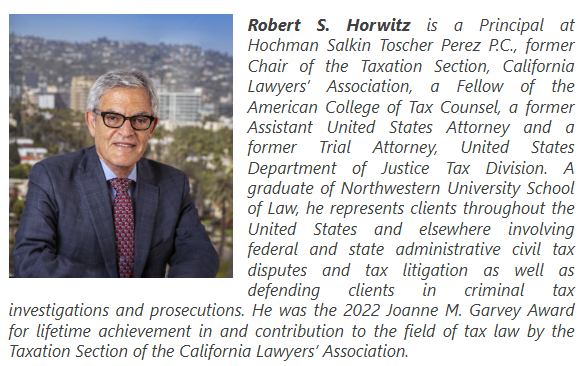

Robert S. Horwitz is a Principal at Hochman Salkin Toscher Perez P.C., former Chair of the Taxation Section, California Lawyers’ Association, a Fellow of the American College of Tax Counsel, a former Assistant United States Attorney and a former Trial Attorney, United States Department of Justice Tax Division. A graduate of Northwestern University School of Law, he represents clients throughout the United States and elsewhere involving federal and state administrative civil tax disputes and tax litigation as well as defending clients in criminal tax investigations and prosecutions. He was the 2022 Joanne M. Garvey Award for lifetime achievement in and contribution to the field of tax law by the Taxation Section of the California Lawyers’ Association.

We are honored and pleased to announce that ten (10) of our Principals have earned a distinguished place in the Lawdragon 500 Leading Global Tax Lawyers. Our firm has one of the deepest and most experienced benches in the civil and criminal tax controversy field and we are proud of such recognition. Lawyers are selected for this honor based upon their exceptional work in critical tax areas, such as complex civil and criminal tax controversies and litigation and the nuanced challenges faced by high-net-worth individuals.

Our Principals included in this prestigious recognition are:

Steven Toscher is the Managing Principal of the law firm, and specializes in civil and criminal tax controversy and litigation. Mr. Toscher is a Certified Tax Specialist in Taxation, the State Bar of California Board of Legal Specialization, a Fellow of the American College of Tax Counsel and has received an “AV” rating from Martindale Hubbell. Mr. Toscher serves as Co-Chair of the UCLA Tax Controversy Institute and Co-Chair of the ABA Criminal Tax Fraud and Tax Controversy Conference. Mr. Toscher is a frequent lecturer and author on tax controversy and litigation topics and is a co-authorof the BNA Portfolio, Tax Crimes.Mr. Toscher was the 2018 recipient of the Joanne M. Garvey Award, given annually to recognize lifetime achievement and outstanding contributions to the field of tax law by a senior member of the California tax bar. Mr. Toscher is also the recipient the USD School of Law Richard Carpenter Excellence in Tax Award. In 2024 Mr. Toscher was the recipient of the prestigious Jules Ritholz Memorial Merit Award presented by the Civil and Criminal Tax Penalties Committee of the Taxation Section of the American Bar Association, recognizing tax lawyers who have demonstrated outstanding dedication, achievement and integrity in the field of civil and criminal tax controversies. For more information, please contact Steven Toscher at toscher@taxlitigator.com.

Dennis Perez was formerly a senior trial attorney with District Counsel, Internal Revenue Service, in Los Angeles, California. Mr. Perez is a Certified Tax Specialist, California State Bar Board of Certification and is also a Fellow of the American College of Tax Counsel. He frequently lectures on advanced civil and criminal tax topics at seminars and before national, state and local bar associations and accountancy groups. Mr. Perez is a co-author of the BNA Portfolio, Tax Crimes, served as the Chair of the Los Angeles Lawyer Magazine Editorial Board and is the first recipient of the Los Angeles Lawyer Sam Lipsman Service Award for outstanding service to the Los Angeles Lawyer Magazine. He is past Chair of the Tax Procedure and Litigation Committees of the Taxation Sections of the State Bar of California and the Los Angeles County Bar Association. Mr. Perez is past President of the Alumni Board for the UCLA School of Law and has served as an Adjunct Professor, Golden Gate University, Graduate School of Taxation. For more information, please contact Dennis Perez at perez@taxlitigator.com

Sandra R. Brown specializes in criminal tax investigations, grand jury matters, litigation and appeals, as well as representing and advising taxpayers involved in complex and sophisticated civil tax controversies, including sensitive-issue audits and administrative appeals, as well as civil litigation. Prior to joining the firm, Ms. Brown served as the Acting United States Attorney, First Assistant United States Attorney; and Chief of the Tax Division in the Office of the U.S. Attorney, Central District of California. During her 27 years as a trial lawyer, she personally handled over 2,000 tax cases on behalf of the United States, including nationally significant civil tax cases such as two Supreme Court decisions and a multitude of published 9th Circuit decisions, as well as a broad range of equally noteworthy criminal tax cases. Ms. Brown obtained her LL.M. in Taxation from the University of Denver, is a fellow of the American College of Tax Counsel, Vice-Chair of the ABA’s Section of Taxation’s Criminal and Civil Tax Penalties Committee, Co-Chair of the UCLA Tax Controversy Institute, Co-Chair of the ABA Criminal Tax Fraud and Tax Controversy Conference, an ABA Loretta Collins Argrett Fellowship Mentor, and is a frequent lecturer and author on tax controversy topics, including international compliance matters. Ms. Brown has been recognized as one of California’s top 100 leading women lawyers and most recently, the recipient of USD School of Law’s Richard Carpenter Excellence in Tax Award and honored at the California Lawyers Association Tax Bar and Tax Policy 2024 Toast to Women in Tax. For more information, please contact Sandra Brown at brown@taxlitigator.com.

Evan J. Davis specializes in handling federal and state criminal and civil tax investigations/exams, white-collar defense, cryptocurrency clients, and civil and criminal appellate matters including having litigated the In re Grand Jury attorney-client privilege matter before the US Supreme Court in 2023. Prior to joining the firm as a Principal in 2016, Mr. Davis spent more than seven (7) years as a DOJ Tax civil litigator and then eleven (11) years as an AUSA in the Office of the U.S. Attorney (C.D. Cal), including 3 years handling civil and criminal tax cases and 8 years as a white-collar prosecutor handling tax and other fraud cases from investigation through jury trial and appeal. As an AUSA, Evan served as the Bankruptcy Fraud coordinator, Financial Institution Fraud coordinator, and Securities Fraud coordinator. During his tenure with the Government, among other awards, Mr. Davis received the Attorney General’s Award for Distinguished Service, the Attorney General’s highest litigation award. Mr. Davis is a fellow of the American College of Tax Counsel and a graduate of Cornell Law School, Order of the Coif, magna cum laude. For more information, please contact Evan Davis at davis@taxlitigator.com.

Robert S. Horwitz represents clients throughout the United States and elsewhere involving federal and state administrative civil tax disputes and tax litigation as well as defending clients in criminal tax investigations and prosecutions. Mr. Horwitz is a former Chair of the Taxation Section, California Lawyers’ Association, a Fellow of the American College of Tax Counsel, a former Assistant United States Attorney and a former Trial Attorney, United States Department of Justice Tax Division. Mr. Horwitz was the 2022 Joanne M. Garvey Award for lifetime achievement in and contribution to the field of tax law by the Taxation Section of the California Lawyers Association. Mr. Horwitz is an Order of the Coif graduate of Northwestern University Law School. For more information, contact Robert Horwitz at horwitz@taxlitigator.com.

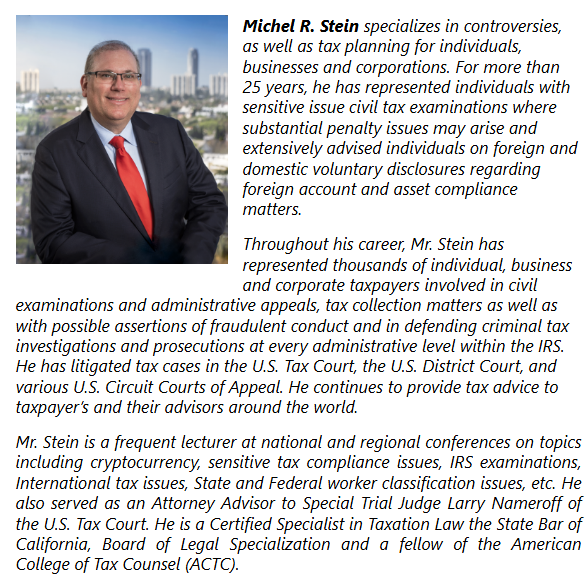

Michel R. Stein has for more than 25 years represented individuals with sensitive issue tax examinations where substantial penalty issues may arise and extensively advised individuals on foreign and domestic voluntary disclosures regarding foreign account and asset compliance matters. He continues to provide tax advice to taxpayer’s and their advisors around the world. Mr. Stein specializes in tax controversies, as well as tax planning for individuals, business entities, and corporations, and has represented many hundreds of individuals, businesses and corporate taxpayers involved in civil examinations and administrative appeals, tax collection matters, as well as the assertions of fraudulent conduct, and in defending civil and criminal tax investigations and prosecutions at every administrative level within the IRS and Franchise Tax Board. Mr. Stein has litigated tax cases in the U.S. Tax Court, U.S. District Court, California Superior Court, and the U.S. Circuit Court of Appeals. Mr. Stein is also a frequent lecturer at national and regional conferences on topics including cryptocurrency, tax court litigation, sensitive tax compliance issues, IRS examinations, international tax issues, partnership examination issues, and state and federal worker classification issues and residency matters, among many other topics. He served as an Attorney Advisor to Special Trial Judge Larry Nameroff of the U.S. Tax Court, following his LLM in Taxation from NYU School of Law. He is a Certified Specialist in Tax Law for the State Bar of California, Board of Legal Specialization, and a fellow of the American College of Tax Counsel (ACTC). For more information, please contact Michel Stein at stein@taxlitigator.com.

Cory Stigile specializes in tax controversies as well as business and international tax. His representation includes federal and state tax controversy matters, including sensitive tax-related examinations and investigations for individuals, partnerships, limited liability companies and corporations. Mr. Stigile’s practice also includes complex civil tax examinations, administrative appeals and tax collection proceedings (where he is widely respected for achieving meaningful resolutions of difficult tax collection issues). He has litigated cases in the U.S. Tax Court, the U.S. District Court, the Court of Federal Claims and the 9th Circuit Court of Appeals. Mr. Stigile is a Certified Specialist, Taxation Law, The State Bar of California, Board of Legal Specialization and a fellow of the American College of Tax Counsel (ACTC). Mr. Stigile is also a CPA licensed in California. He is an active volunteer with CalCPA and the AICPA, and is the President of PADI Foundation. For more information, please contact Cory Stigile at stigile@taxlitigator.com.

Edward M. Robbins, Jr. has been a Principal with the law firm since 2004. Mr. Robbins represents clients in civil and criminal tax litigation and in tax disputes and controversies before the Internal Revenue Service and in federal and state court matters. Before entering private practice, Mr. Robbins was an Assistant United States Attorney with the Central District of California, Tax Division. Mr. Robbins left the government after ten years serving as the Chief of the Tax Division, six years as Assistant Division Chief, nine years as Assistant United States Attorney, and 4 years as a District Counsel attorney with the IRS Chief Counsel office in Los Angeles. Mr. Robbins has an LLM in Taxation from the University of San Diego. He is a Certified Specialist in Tax Law for the State Bar of California, Board of Legal Specialization, and a fellow of the American College of Tax Counsel (ACTC). Mr. Robbins has served as an Adjunct Professor at both Golden Gate University School of Law and Loyola Law School. For more information, please contact Edward Robbins, Jr. at EdR@taxlitigator.com.

Avram Salkin is a founding member of the firm. He has over fifty (50) years of extensive experience in resolving complex Federal and state tax controversies and disputes, in structuring and negotiating complex transactional matters (including the acquisition and disposition of real estate and businesses), family wealth planning, estate planning and probate. Recognizing a lifetime of achievements and contributions to the field of taxation, Mr. Salkin has been honored with the Dana Latham Award (Los Angeles County Bar Association), the Joane M. Garvey Award (Taxation Section of the State Bar of California), and the Bruce I. Hochman Award (UCLA Tax Institute). Mr. Salkin served as a Member of the Board of Governor’s for the Beverly Hills Bar Association, was Vice-Chair of the Tax Advisory Commission for the California State Bar Board of Legal Specialization, and has served as the Tax Articles Editor for the Los Angeles County Bar Journal. Mr. Salkin holds an “A-V” rating from Martindale-Hubbell.

Lacey Strachan, a Principal with the firm, focuses her practice on civil and criminal tax litigation, representing high-net-worth individuals, estates, fiduciaries, and businesses in high-stakes disputes with federal and state taxing authorities. Her extensive experience spans all stages of tax controversy, from audit and administrative appeals to trial and appeal, including certiorari briefing before the U.S. Supreme Court. Ms. Strachan has achieved notable results for clients in cases involving a broad range of substantive tax issues, including cases of first impression. Ms. Strachan serves on the Editorial Board for Los Angeles Lawyer magazine and is a skilled advocate and persuasive writer, known for distilling complex factual and legal issues into succinct and compelling arguments. Ms. Strachan is particularly respected for her work on cases involving complex valuation issues, drawing on a background in economics and years of experience working closely with valuation experts. She brings analytical precision and a deep understanding of valuation methodology to disputes involving the value of closely held businesses, intellectual property, real estate, and other hard-to-value assets. She was a member of the Tax Court trial team responsible for the Estate of Michael Jackson prevailing against the IRS in its landmark estate tax valuation case, reducing the asserted tax liability by hundreds of millions of dollars. For more information, please contact Lacey Strachan at strachan@taxlitigator.com.

We are pleased to announce thatMichel R. Stein, Robert S. Horwitz and Sebastian Voth will be speaking at the upcoming Strafford webinar, Federal and State Residency Issues webinar, Thursday, May 22, 2025, 10:00 a.m. – 11:30 a.m. (PST).

This webinar will guide tax professionals and advisers on the latest IRS examination guidance on U.S. residency and California residency issues. The panel will discuss federal and state tax residency rules, California residency issues, income allocation issues in the residency context, managing residency audits, and best practices for advising clients who are considering leaving California. The IRS LB&I unit has issued examination guidance focused on taxpayer residency. California state tax residency rules, and an increase in residency audits and enforcement require tax professionals to know state residency and income allocation issues, so they can properly advise their clients when these issues arise.

Legal Disclaimer. This Report only provides general information about the law and does not, under any circumstances, constitute legal advice in any manner. The facts of each situation are unique and you should not act or refrain from acting in any manner based on any information contained or referenced in this Report at any time without first obtaining the advice of competent professional legal counsel. This site contains links to third-party internet sites. We are not responsible in any manner for, and make no representations or endorsements of any kind whatsoever with respect to, any third-party internet sites or with respect to any information, products or services that such internet sites might offer or provide.