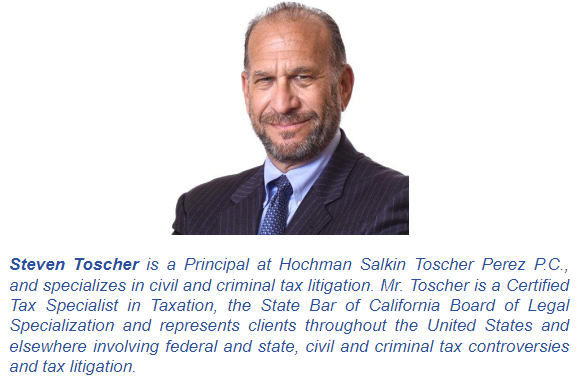

Steven Toscher was quoted in recent Tax Notes article discussing the IRS increased enforcement efforts concerning Maltese Pension Plans. One of his primary concerns was due process considerations when the IRS pursues a criminal investigation in an area of tax law which is not very clear.

“A criminal case based on a substantively debatable return position could be legally stillborn, he said . . . The IRS and Justice Department shouldn’t be prosecuting cases turning on unclear law, Toscher said . . . This Supreme Court would likely be amenable to conviction challenges if the agencies managed to convict someone for taking a position on which the law is uncertain, he said . . . The need for the competent authority agreement clarification will likely bolster that defense, according to Toscher.”

We are pleased to announce that Michel Stein, Edward Robbins, Jr. and Sandra Brown will be speaking at the upcoming CalCPA webinar “Form 8300 Reporting/Cash Intensive Business Audits,” Tuesday, July 18, 2023, 9:00 a.m. – 10:00 a.m. (PST).

The law requires that trades and businesses report cash payments of more than $10,000 to the federal government by filing Form 8300. This course will explain the Form 8300 filing of obligations of those accepting cash payments in their businesses, best practices surrounding the filing of the Forms 8300, the current civil and criminal enforcement environment surrounding Form 8300 non-compliance, and the voluntary disclosure and mitigation practices surrounding the non-compliant. Do not be caught unprepared!

We are very pleased to announce that Sandra R. Brown has been appointed vice chair of the Section’s Civil and Criminal Tax Penalties Committee for the 2023-2024 term. Sandra’s selection as a committee vice chair and as a Section leader represents recognition by her peers of her abilities and contributions to the work of the Section.

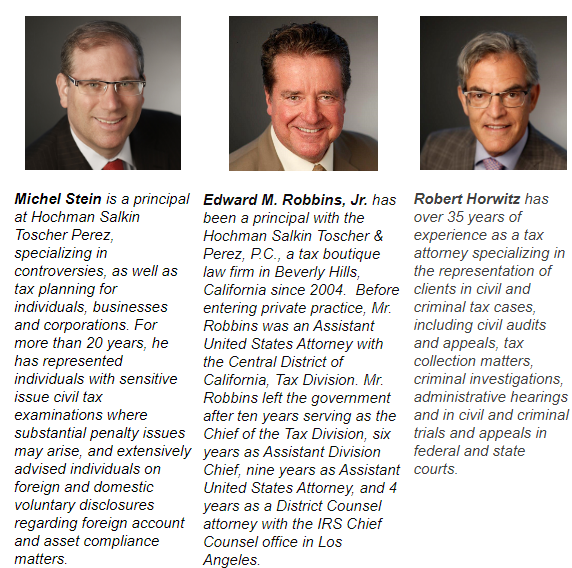

Sandra has over 30 years of experience as a tax attorney specializing in the representation of clients in civil and criminal tax cases, including civil audits and appeals, tax collection matters, criminal investigations, and in civil and criminal trials and appeals in federal courts. Prior to joining Hochman Salkin Toscher Perez, P.C., in 2018 as a principal, Sandra was the Acting United States Attorney, the First Assistant United States Attorney, and the Chief of the Tax Division for the United States Attorney’s Office, Central District of California.

We are also pleased to announce that Jonathan Kalinski has been selected as co-chair of the Legislative & Administrative Developments Sub-Committee of the Civil and Criminal Penalties Committee for the 2023-2024 term.

Jonathan specializes in both civil and criminal tax controversies as well as sensitive tax matters including disclosures of previously undeclared interests in foreign financial accounts and assets and provides tax advice to taxpayers and their advisors throughout the world. Jonathan has considerable experience handling complex civil tax examinations, administrative appeals, and tax collection matters. Prior to joining the firm, he served as a trial attorney with the IRS Office of Chief Counsel litigating Tax Court cases and advising Revenue Agents and Revenue Officers on a variety of complex tax matters. Jonathan Kalinski also previously served as an Attorney-Adviser to the Honorable Juan F. Vasquez of the United States Tax Court.

The Internal Revenue Service has long had the power to issue and enforce administrative summonses for the purpose of “ascertaining the correctness of any return … determining the liability of any person for any internal revenue tax … or to collect any such liability.” See Reisman v. Caplin, 375 U.S. 440 (1964). While the courts and the IRS recognized that a taxpayer or an interested party had a right to intervene in an action brought by the IRS to enforce a summons, prior to the 1976 enactment of Internal Revenue Code §7609, there was no legal requirement that notice of a summons be given to a person identified in the summons (other than the summoned person).

IRS Special Agents fanned out throughout the United States on June 30, seeking to interview promoters and clients of a “Maltese individual retirement arrangement” that for the past three years has earned a spot on the IRS’s Dirty Dozen tax promotions list. These are simply the first public actions in what will doubtless be a massive and worldwide investigation.

In 2021, the IRS first announced (IRS wraps up its 2021 “Dirty Dozen” scams list with warning about promoted abusive arrangements | Internal Revenue Service) that “. . . some U.S. citizens were relying on an interpretation of the US-Malta tax treaty to assert that contribution of appreciated property to a Maltese pension plan could contribute the appreciated property to the pension plan, which could then sell the property and distribute the proceeds, all tax-free . . .” The treaty’s plain language appears to permit this favorable treatment, but the IRS thinks this result wasn’t intended, is too good to be true, and therefore everyone must understand that the treaty can’t mean what it appears to say. A few months later, the IRS and Malta tax authority announced in a CAA (malta-competent-authority-arrangement-pension-funds.pdf (irs.gov)) a joint interpretation of the US-Malta tax treaty that sought to foreclose the promoters’ and taxpayers’ argument in favor of the Malta pension plan promotion. The IRS made sterner Dirty Dozen announcements in 2022 and 2023, and on June 7, 2023, the IRS published a proposed rule to make Maltese pension plan arrangements “listed transactions” that require taxpayers to disclose them on IRS forms. Thirty-six other transactions have previously been added to this IRS naughty list, but the IRS generally stops there and treats such transactions exclusively as civil matters subject to harsh penalties. Listed Transactions | Internal Revenue Service (irs.gov)

However, the most recent listed transaction, in 2017, has generated substantial criminal investigations and indictments, namely syndicated conservation easements. Unfortunately for many taxpayers and promoters who became clients of our firm and other criminal tax experts, the IRS opened criminal investigations of conservations easements and has ensnared primarily accountants and other professionals. One listed transaction becoming multiple criminal investigations is an anomaly; two consecutive listed transactions turning criminal is now a trend.

Choosing to open a wide-ranging criminal investigation of sophisticated tax transactions is a rare step, one the government does not take lightly. The volume of scarce resources devoted to such cases is staggering, with dozens of agents and prosecutors spending years poring over emails, seeking foreign evidence through Mutual Legal Assistance Treaty and Exchange of Information requests, facing well-resourced and well-represented targets who in turn have relied on professionals, and facing the daunting task of explaining to a jury why this complicated transaction was an obvious fraud. We often see the government has bitten off more than it can chew on such cases, although it has had success in obtaining pleas from some involved in syndicated conservation easements. However, the hard task of taking one of those cases to a jury has not occurred, yet the IRS and Department of Justice have opened another front on promoters of allegedly abusive tax schemes. In the case of the Malta IRAs, any criminal case based on the promotion being “too good to be true” should be dead on arrival, so the IRS should have good reason to think that promoters and/or clients are making knowingly false statements to the IRS that goes beyond a dispute about the substance versus form of the tax treaty.

If you or a client are in the unfortunate position of having participated in or promoted the Malta IRA program, then seek advice from an experienced civil and criminal tax counsel now. And if the IRS has already knocked on your door, remember that they aren’t there to simply hear what you have to say, but instead are looking to put together a criminal case against anyone they think worthy of charges and that could include you. Most often, they target the promoters, but not always. There’s only one way to be safe in this situation: politely decline to answer questions without having counsel present. For those who have already been contacted and those who merely participated and have not been contacted yet, experienced counsel will address any immediate criminal issues and discuss filing amended returns or participating in various IRS programs such as the Voluntary Disclosure program and Streamlined procedure, which our firm has successfully completed for countless clients over the years.

Hochman Salkin Toscher Perez P.C., Homepage – Taxlitigator, is recognized as the pre-eminent civil and criminal tax litigation firm on the West Coast. Nearly all its principals spent years working as civil litigators and/or criminal prosecutors for one or more of the Department of Justice Tax Division, U.S. Attorney’s Office, or the IRS, and we have achieved remarkable success in helping clients avoid criminal charges, steering clients through sensitive audits, settling complex civil matters, and winning even difficult civil and criminal cases at trial and on appeal.

EVAN J. DAVIS – For more information please contact Evan Davis – davis@taxlitigator.com or 310.281.3288. Mr. Davis has been a principal at Hochman Salkin Toscher Perez P.C. since November 2016. He spent 11 years as an AUSA in the Office of the U.S. Attorney (C.D. Cal), spending three years in the Tax Division where he handed civil and criminal tax cases and eight years in the Major Frauds Section of the Criminal Division where he handled white-collar, tax, and other fraud cases through jury trial and appeal. As an AUSA, he served as the Bankruptcy Fraud coordinator, Financial Institution Fraud coordinator, and Securities Fraud coordinator. Among other awards as a prosecutor, he received an award from the CDCA Bankruptcy Judges for combatting Bankruptcy Fraud and the U.S. Attorney General awarded him the Distinguished Service Award (DOJ’s highest litigation award) for his work on the $16 Billion RMBS settlement with Bank of America. Before becoming an AUSA, Mr. Davis was a civil trial attorney in the Department of Justice’s Tax Division in Washington, D.C. for nearly 8 years, the last three of which he was recognized with Outstanding Attorney awards. He is a magna cum laude and Order of the Coif graduate of Cornell Law School and cum laude graduate of Colgate University.

Mr. Davis represents individuals and closely held entities in federal and state criminal tax (including foreign-account and cryptocurrency) investigations and prosecutions, civil tax controversy and litigation, sensitive issue or complex civil tax examinations and administrative tax appeals, and white-collar criminal investigations including campaign finance, FARA, money laundering, and health care fraud.

We are pleased to announce that Michel Stein along with Caroline Ciraolo, Phillip Colasanto and Daniel Price will be speaking at the upcoming CPA Academy webinar “The Future of Voluntary Disclosures: Coming in From the Cold,“Wednesday, June 28, 2023, 9:00 a.m.– 10:00 a.m. (PST).

For more than 70 years, the IRS maintained a voluntary disclosure policy designed to encourage taxpayers to come in from the cold and self-report non-compliance. In 2018, the voluntary disclosure program was updated to provide new procedures. In its most recent annual report, the Taxpayer Advocate Service noted that the new procedures are substantially more onerous and uncertain than the old procedures and may discourage taxpayers from stepping forward to self-disclose.

This session will discuss the latest voluntary disclosure developments, including the application of the updated program to cryptocurrency, and provide suggestions on how practitioners should advise their clients to make the best use of the new voluntary disclosure procedures.

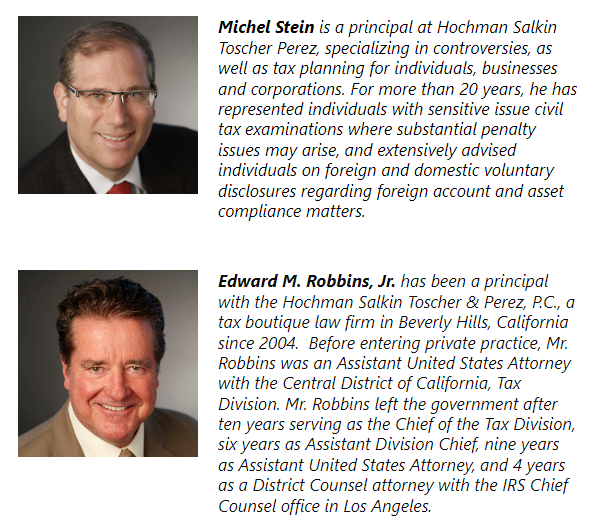

We are pleased to announce that Michel Stein, Edward Robbins, Jr. and Robert Horwitz will be speaking at the upcoming Strafford webinar “Foreign Information Return Penalties After Farhy: Case Review and Updates, Penalty Abatements, Refund Claims,“Tuesday, June 27, 2023, 10:00 a.m.– 11:50 a.m. (PST).

The Supreme Court, in Bittner v. United States, limited the imposition of FBAR filing penalties to a single penalty per form rather than penalizing the taxpayer for each foreign account, astronomically reducing the amount the IRS can assess taxpayers for improperly filing these information returns. This decision, and the more recent outcome in Farhy v. Commissioner, stand in stark contrast to the many cases over the years imposing astounding penalties for non and late filing of foreign information returns.

In Farhy v. Commissioner 160 T.C. No. 6 (T.C. Apr. 3, 2023), the Tax Court ruled that the IRS did not have the authority to assess and collect penalties under IRC Section 6038(b) for failure to file Forms 5471. The IRS will likely appeal the Farhy decision but now would need to file a civil action to collect these penalties. In the interim, international tax advisers must reassess the status of late and non-filed foreign information reports. The ramifications of this ruling could apply to other forms, including Forms 5472, 8858, 8938, 926, and perhaps even the 3520.

For tax practitioners bombarded with multiple penalties in increments of, and no less than, $10,000 each for multiple clients, the Farhy decision offers the opportunity for substantial refunds of erroneously assessed penalties. It also opens the door to a multitude of questions on eligibility and applying for relief.

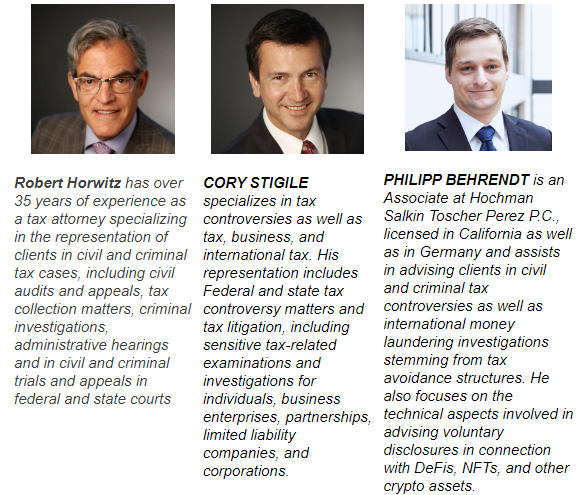

We are pleased to announce that Robert Horwitz, Cory Stigile and Philipp Behrendt will be speaking at the upcoming Strafford webinar “Partnership Losses in Excess of Basis: Preparing for the IRS Audit Campaign,“Tuesday, June 20, 2023, 10:00 a.m.– 11:50 p.m. (PST).

In February 2022, the IRS announced a partnership campaign to include audits of partners’ deductions of flow-through losses from partnerships. The Service believes that partners are deducting losses in excess of basis rather than suspending these losses when required. The IRS heightened its ability to track partners’ capital by implementing requirements to report negative tax basis capital in 2019, all partners’ capital accounts beginning in 2020, and added disclosures for Section 704(c) built-in gains and losses. The IRS is using data analytics to identify partnerships that are most likely noncompliant.

Practitioners who have been scrambling to meet these added reporting requirements must prepare to defend these positions and the calculations reported. Determining a partner’s outside basis, including whether tax basis capital has been appropriately captured and a partner’s share of liabilities, is complicated. Recent reporting rules have led to the discovery of allocation errors.

Pass-through entity advisers need to prepare for upcoming examinations and know how to handle audits of pass-through entities. Listen as our panel of IRS partnership examination experts explains how to properly maintain and support partners’ basis in partnerships and how to defend these calculations when representing partners.

I am very pleased to announce and ask you to Save the Date for this years ABA National Institute on Criminal Tax Fraud & Tax Controversy to be held December 7-9, 2023 at Wynn, Encore in Las Vegas, Nevada. I am honored again to be serving as Co-Chair with Kathryn Keneally. We look forward to the best programs in the nation on civil and criminal tax controversy and litigation and well—Las Vegas.

The National Institute on Criminal Tax Fraud and the National Institute on Tax Controversy, combined together in one event, comprises the yearly gathering of the criminal tax controversy and criminal tax defense bar. The program brings together high-level government representatives, judges, corporate counsel, and private practitioners engaged in all aspects of tax controversy, tax litigation, and criminal tax prosecutions and defense.

HOCHMAN SALKIN TOSCHER PEREZ P.C. is proud to be recognized by Chambers and Partners as one of only three top tier law firms in its U.S. 2023 High Net Worth Guide in the category of Tax: Private Client, as well as a top firm nationwide in the Tax Controversy and Tax Fraud areas.

Chambers concluded that HOCHMAN SALKIN TOSCHER PEREZ P.C., is “a superb firm for tax controversy matters” and “has a hugely impressive track record in tax controversy, alongside criminal and civil litigation at both state and federal levels.” Chambers quotes clients as noting: “They’re my go-to firm for sophisticated tax controversy matters.” “The firm’s lawyers have deep, substantive knowledge and key connections throughout the California federal bench.“

In addition to the recognition of the firm, Steven Toscher, Dennis Perez and Sandra R. Brown were named top tier lawyers in the 2023 High Net Worth Guide Tax: Private Client USA Rankings. Steven was also ranked as a top Tax Fraud litigator for a third consecutive year.

Chambers reports that Steve “is noted for his experience advising clients on contentious tax matters, including IRS and DOJ litigation. He regularly works with corporations and individuals.” “He is a well-regarded tax practitioner who advises clients on sensitive issues, including criminal tax fraud investigations.” “Steve Toscher has an excellent reputation as a litigator.“

Steve has been representing clients for almost 40 years before the United States Tax Court, the Federal District Courts, the Internal Revenue Service, the Tax Division of the U.S. Department of Justice and the Offices of the United States Attorney, numerous state taxing authorities in federal and state court litigation and appeals. He is a Certified Specialist in Taxation by the State Bar of California Board of Legal Specialization and is often ranked in California as well as nationwide as a top tax lawyer including being honored by the Taxation Section of the California State Bar with the 2017 Joanne M. Garvey Award.

Dennis Perez represents high-net-worth clients in domestic tax examinations and administrative appeals as well as in civil and criminal litigation. As noted by Chambers, “He is one of the strongest practitioners in the country on the foreign reporting space.” “He’s a great practitioner. He is definitely somebody I can recommend in this area.”

A former senior trial attorney with the IRS District Counsel in Los Angeles, California, Mr. Perez has, for more than 35 years, represented and advised clients in foreign and domestic civil tax examinations and administrative appeals where substantial civil income tax and penalty issues may arise, and he has extensive experience in representing clients in criminal tax fraud investigations and prosecutions. He is also a Certified Specialist in Taxation, the State Bar of California Board of Legal Specialization. Mr. Perez is the first-ever recipient of the Los Angeles Lawyer Sam Lipsman Service Award.

Sandra R. Brown represents high-net-worth individuals and businesses in a broad range of civil and criminal tax investigations. Chambers reports that “She is a very good attorney. She is knowledgeable, technical and knows her stuff.” “Sandra Brown is exceptional. She has a wealth of experience she is really clever and a very good strategist. I would happily refer a case to her.”

In more than 30 years as a tax litigator, Ms. Brown has a vast depth of experience in complex civil and criminal tax matters, having personally handled over 2,000 cases before the United States District Courts, the Ninth Circuit Court of Appeals, the United States Bankruptcy Court, the United States Bankruptcy Appellate Panel and the California Superior Court. Those cases included nationally significant civil tax cases such as two Supreme Court decisions and a multitude of published 9th Circuit decisions. Ms. Brown received her LL.M. in Taxation from the University of Denver, served as the Acting U.S. Attorney for the Central District of California, Chief of the Tax Division, and, in 2021, was named a Top Women Lawyer in California.

HOCHMAN SALKIN TOSCHER PEREZ P.C., enjoys an unparalleled reputation for excellence and integrity in the tax community. For more than 60 years, the firm has been serving clients throughout the United States with federal and state civil tax litigation, defense of criminal tax prosecutions, and tax disputes with the federal, state and local taxing authorities. More information about the firm and our attorneys is available at https://www.taxlitigator.com/

Legal Disclaimer. This Report only provides general information about the law and does not, under any circumstances, constitute legal advice in any manner. The facts of each situation are unique and you should not act or refrain from acting in any manner based on any information contained or referenced in this Report at any time without first obtaining the advice of competent professional legal counsel. This site contains links to third-party internet sites. We are not responsible in any manner for, and make no representations or endorsements of any kind whatsoever with respect to, any third-party internet sites or with respect to any information, products or services that such internet sites might offer or provide.