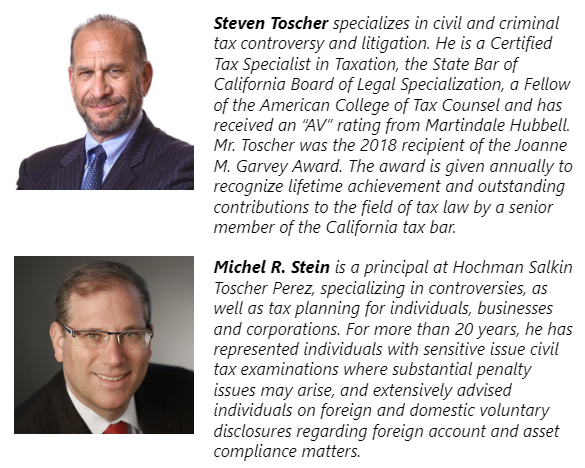

We are pleased to announce that Steven Toscher and Michel R. Stein, will be speaking at the upcoming CalCPA webinar “Handling the New IRS Global High Wealth Examinations 2023,” Tuesday, November 14, 2023, 9:00 a.m. – 10:00 a.m. (PST).

The Global High Wealth Group is an industry group created by the IRS LB&I in 2009. The purpose of the Global High Wealth Group (also known as the “Wealth Squad”) is to bring together an IRS team of specialists to conduct detailed examinations of complex returns of high wealth individuals and their related entities. The IRS with updated Internal Revenue Manual provisions governing high wealth audits is poised to start the examination of hundreds of high net-worth taxpayers and large partnerships. Recent IRS announcements state that additional resources provided by the Inflation Reduction Act of 2022 will be laser focused on high wealth persons and examinations, which typically involve pass-through businesses, related trusts, foreign holdings, tiered partnerships, and related tax-exempt organizations.

The program’s learning objectives include:

Understanding the Global High Wealth Group audit program

Learn strategies to minimize risk from Global High Wealth Group audits

Master techniques in handling and advising clients examined by the Global High Wealth Group

We anticipate that attendees will: Better understand the “Wealth Squad” examination process, Know what foreign and domestic audits issues will be scrutinized during a “Wealth Squad” examination, Decipher “Wealth Squad” document requests and summonses, and more easily identify key strategies to minimize exposure from a “Wealth Squad” examination.

We are pleased to announce that two of our partners will be speaking at the upcoming NYU 82nd Institute on Federal Taxation being held at the Clairmont Resort and Spa, Berkeley, California on November 12-17, 2023.

We have an excellent lineup of programs –

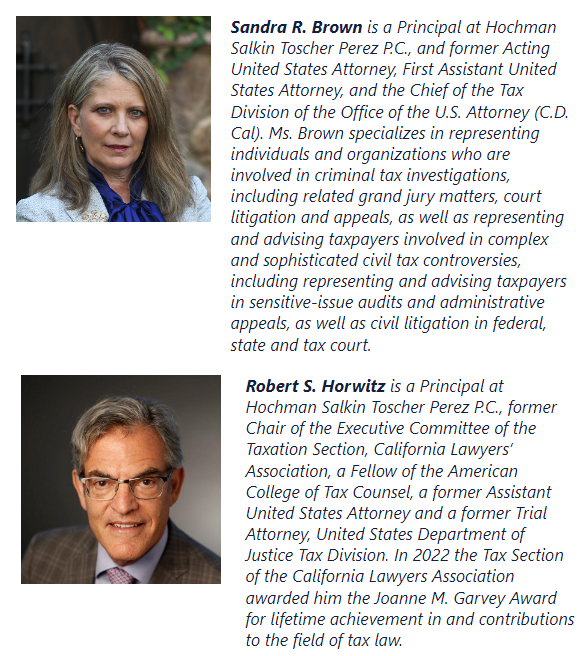

From the Experts: Tax Controversy and Tax Litigation – Civil & Criminal Tax Update Featuring Sandra Brown Sunday, November 12th at 1:15 p.m. to 3:45 p.m.

How Far Can You Go? Ethical and Penalty Issues in Everyday Practice Featuring Michel R. Stein Thursday, November 16th at 5:15 p.m. to 6:55 p.m.

This year’s program provides unparalleled educational and professional development opportunities delivered by a diverse and distinguished faculty of recognized tax and wealth-transfer authorities with a positive approach to current and practical subjects.

While the Institute is designed primarily to serve as a forum where tax and wealth transfer oriented people may freely exchange ideas on practical problems, professional status is not a prerequisite for registration. This program is designed for attorneys, accountants, financial planners, planned giving professionals, bank and trust administrators, insurance agents, elder law specialists, non-profit administrators, wealth management professionals, enrolled agents, educators, and others who would benefit from high quality continuing education. The highest level of learning has been the hallmark of prior Institutes and we shall endeavor to again maintain this standard.

The Taxation Section of the California Lawyers Association presented Taxpayer Advocate Erin Collins with the Joanne M. Garvey Award for her lifetime achievement in taxation. Introducing Erin and pictured above is her husband Edward Robbins. Prior recipients of this prestigious award include members and former members of Hochman Salkin Toscher Perez, P.C., Robert Horwitz, former Commissioner Charles P. Rettig and Steven Toscher.

We are pleased to announce that Cory Stigile will be speaking at the upcoming 2023 Oregon State Tax Update – IRS Global High Wealth Audits webinar, November 27, 2023, 8:30 a.m. – 3:30 p.m. (PST).

The presentation will include global high wealth audits interrelationship with BBA procedures ethical issues.

This webinar will also present on the following:

Sales Tax Fundamentals Industry specific issues

Doing business in other states

Recent developments Oregon Corporate Activity Tax Review of corporate tax rates and rules

Newly-enacted and anticipated corporate tax changes

Recent case law Oregon Paid Leave Summary of benefits, employee eligibility and program start date

Employer obligations and funding process

Notice and reporting requirements

Reasons for qualified leave Differences with FMLA/OFLA Available alternatives Portland Metro Taxes Portland Arts Education

Access Income Tax (Arts Tax) Portland Business License Tax (including related programs) Multnomah County business income tax Multnomah County Preschool for All (PFA) personal income tax Metro Supportive Housing Services (SHS) business income tax Metro Supportive Housing Services (SHS) personal income tax

Introduction: The term “Release the Kraken” may bring to mind its origin in the movie “Clash of the Titans,” but the real battle is now in the realm of tax compliance. In a recent development that could have significant implications for cryptocurrency users, one of the largest cryptocurrency exchanges, Kraken, has notified its customers that it will release user data to the IRS. This follows a recent district court ruling enforcing a 2021 John Doe summons issued by the IRS to Kraken’s parent company to obtain information on digital asset transactions between 2016 and 2020.[i] While the court’s decision limited the scope of the data Kraken must provide, it remains crucial for cryptocurrency investors to understand the potential implications of this disclosure for their tax returns.

What information will be shared: Kraken will be supplying “limited data” on its users to the IRS, as mandated by the court. This data will include information on accounts with at least $20,000 worth of transactions in any one year between January 1, 2016, and December 31, 2020, and will include user details such as name, date of birth, tax identification number, address, phone number, email address, and transaction data from the 2016-2020 period.

CP2000 Notices: One of the immediate consequences of this data release could be the issuance of CP2000 notices by the IRS to affected taxpayers. CP2000 notices are sent when the IRS identifies discrepancies between a taxpayer’s reported income and information reported to the IRS by third parties. These notices serve as a preliminary step in the IRS’s efforts to determine whether a taxpayer’s return correctly reports income, gain, deductions, and credits. They often require a response from the taxpayer. See https://www.irs.gov/taxtopics/tc652.

Why You Shouldn’t Ignore CP2000 Notices: It’s crucial to understand that receiving a CP2000 notice should not be taken lightly or ignored. In this case, the data provided by Kraken may be incomplete or may contain inaccuracies, such as missing data, omitted transactions, or misclassifications of income as ordinary or capital gains. Responding to a CP2000 notice is crucial. However, this response must be accurate and timely. It is recommended that taxpayers who receive a CP2000 Notice consult with a tax professional to determine the appropriate response. Ignoring the notice can lead to problems later in down the road.

Possible IRS Actions: While CP2000 notices are one potential outcome, it is essential to be aware that the IRS may also initiate audits or, in rare instances, even criminal investigations based on the data received. These potential actions by the IRS underscore the need for taxpayers who used Kraken to consult with a qualified tax professional.

Taking Action: If you are a Kraken user who may be affected by this data release, you should consider taking the following steps:

Review Your Tax Returns: Assess whether your previous tax returns accurately reflect your cryptocurrency transactions, especially those during the 2016-2020 period.

Consult a Tax Professional: If you suspect any errors or discrepancies in your tax filings, it is advisable to consult with a certified public accountant (CPA) or a tax lawyer who can help you rectify any issues.

Amend Your Tax Returns: If necessary, you may need to amend your tax returns to ensure that your cryptocurrency income is accurately reported. In certain instances, a voluntary disclosure might be required. Your tax professional will be able to navigate you through these intricacies.

Respond to IRS Notices: If you receive a CP2000 notice or any other communication from the IRS, respond promptly and provide the requested information. You may wish to consult with a tax professional, who can interact with the IRS, to address these IRS notices.

Conclusion: While this situation may seem daunting, being proactive in addressing any discrepancies can help you navigate these turbulent waters effectively.

The release of Kraken’s user data to the IRS carries implications for taxpayers who may have had cryptocurrency transactions during the specified period. Being informed and taking appropriate action now can help you avoid potential tax issues in the future. Don’t hesitate to seek professional guidance to ensure your tax returns accurately reflect your cryptocurrency activities and the appropriate action to take if there are errors or inaccuracies.

______________________________

[i]United States v. Payward Ventures, Inc., and its subsidiaries (collectively “Kraken”), Case No. 21-cv-02201-JCS (N.D.Cal.).

We are pleased to announce that two of our partners will be speaking at the upcoming Hawaii Tax Institute 60th Annual Conference being held at the Sheraton Waikiki on November 5–9, 2023.

We have an excellent lineup of programs –

Understanding the Sandbox that All Wealth Transfer Advisors Play In Featuring Sandra Brown

Dual-Purpose Communications in the Tax Context Featuring Evan Davis

Employee Retention Credit Audits and Investigations – The Tsunami is Coming Featuring Sandra Brown

This year’s program provides unparalleled educational and professional development opportunities delivered by a diverse and distinguished faculty of recognized tax and wealth-transfer authorities with a positive approach to current and practical subjects.

While the Institute is designed primarily to serve as a forum where tax and wealth transfer oriented people may freely exchange ideas on practical problems, professional status is not a prerequisite for registration. This program is designed for attorneys, accountants, financial planners, planned giving professionals, bank and trust administrators, insurance agents, elder law specialists, non-profit administrators, wealth management professionals, enrolled agents, educators, and others who would benefit from high quality continuing education. The highest level of learning has been the hallmark of prior Institutes and we shall endeavor to again maintain this standard.

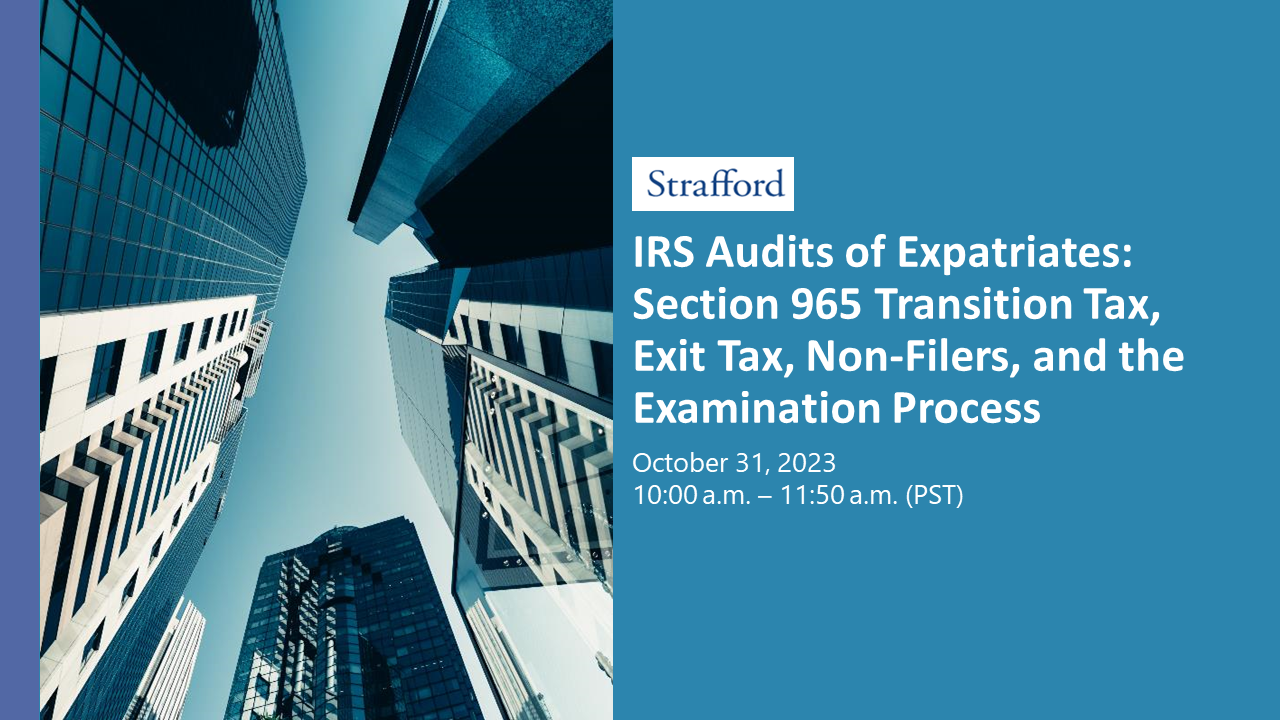

We are pleased to announce that Steven Toscher and Michel Stein, will be speaking at the upcoming Strafford webinar “IRS Audits of Expatriates: Section 965 Transition Tax, Exit Tax, Non-Filers, and the Examination Process” Tuesday, October 31, 2023, 10:00 a.m. – 11:50 a.m. (PST).

The IRS has and continues to audit a higher proportion of expat tax returns. The IRS 2019 Databook revealed that approximately 10 percent of expatriates’ tax returns are selected for audit. Considering the complexity of the returns, this should not be surprising.

The rules for these nonresidents are often the reverse of those for residents. The filing status Married Filing Jointly can require a special election, self-employed taxpayers often are not entitled to deduct expenses, and simple presence in the U.S. for 183 days can trigger capital gains. Remarkably, two-thirds of expats paper file these complicated returns.

In April 2023, the IRS Large Business & International Division released its list of currently active compliance campaigns. A dozen of these issues include campaigns targeting international taxpayers. These audits include expats who filed Form 8854, Initial and Annual Expatriation Statement, as well as those who did not.

Included on the list is its compliance campaign focusing on Section 965 transition tax payments. The Service required these payments by U.S. shareholders of certain foreign corporations on unrepatriated (untaxed) earnings as part of the 2017 Tax Act. The IRS stated that these audits could be expanded to other issues, particularly those relative to the 2017 Tax Act.

However, a major case pending before the U.S. Supreme Court (Moore v. United States, Case No. 22-800) is calling into question this provision on the issue of whether the 16th Amendment authorizes Congress to tax unrealized sums without apportionment among the states. Depending on how the court rules, large portions of the U.S. tax code could become legally uncertain.

Tax professionals and advisers working with individuals who have relocated abroad must understand the issues triggering these IRS audits, prepare clients for these audits, and know how to handle these demanding examinations.

We are pleased to announce that Sandra Brown will be speaking at the upcoming Alvarez& Marsal Tax and Wolters Kluwer Virtual Coffee Talk webinar “Employee Retention Credits” Tuesday, October 31, 2023, 12:00 a.m. – 1:00 p.m. (EST).

The employee retention credit (ERC), enacted as part of the CARES Act, is a US federal tax credit that provides an incentive to employers who continued to employ individuals during the COVID-19 pandemic. Since its enactment, there have been questions as to whether a business qualified and how to interpret what qualified as a full or partial suspension of operations in order to be eligible for the credit. Companies engaged advisors – some of whom were diligent in determining a businesses’ eligibility – though others engaged advisors, whose business models created incentives to take aggressive positions on employee retention credit qualification that likely are not sustainable under audit. The IRS’s focus on fraudulent ERC claims has earned these transactions the #1 spot on the IRS’s annual Dirty Dozen list and has created opportunities for corrective action for those who may have not yet received the claimed credits and are concerned about the legitimacy of their ERC claims. This also puts increased pressure on acquirers in M&A transactions to ensure the appropriate level of diligence was performed, and if not, how buyers can contractually protect themselves in an M&A transaction.

The IRS has recently made big headlines about focusing enforcement initiatives on wealthy individuals, but we have not heard so much about the focus on corporations -until this week. Yes—corporations are part of the tax gap.

The recent IRS announcements regarding new corporate tax compliance initiatives mark the beginning of a new phase in the relationship between the IRS and large corporations. With the agency taking significant steps to ensure that businesses fulfill their tax obligations, it is essential for corporations to understand these initiatives and get ready to deal with the new reality of a greater focus on corporate compliance.

On October 20, 2023, the IRS released its second quarterly update, shedding light on how Inflation Reduction Act (IRA) funds are being utilized and the implementation of priorities. The update unveiled three corporate tax compliance initiatives, underscoring the IRS’s commitment to holding corporations accountable for their tax responsibilities.

1. Transfer Pricing Soft Letter Compliance Alerts for Foreign-Owned Corporations: The IRS is set to send “compliance alerts” to approximately 150 U.S. subsidiaries of foreign corporations, indicating potential misuse of transfer pricing tactics to report diminished profits on domestic activities. These alerts suggest it’s time to take a hard look at the company’s transfer policies and practices and start getting ready to head off or prepare for a transfer pricing examination.

2. Expansion of Large Corporate Compliance Program: In conjunction with its plan to hire 3,700 new revenue agents , the IRS is expanding its large corporate compliance program. The program scrutinizes large corporate taxpayers with substantial assets, meaning average assets of more than $24 billion, and average taxable income of approximately . $526 million per year. The expansion includes initiating an additional 60 audits of major corporations in early 2024 increasing the examination of these businesses. The IRS will apply a combination of artificial intelligence and subject matter expertise in an effort to crack down on noncompliance.

3. Abuse of Repealed Corporate Tax Break: The IRS emphasized its efforts to address what it considers the abuse of the section 199 deduction for domestic production, which was repealed in the 2017 Tax Cuts and Jobs Act. These efforts have borne fruit, highlighted by a significant victory for the IRS in Bats Global Markets Holdings Inc. v. Commissioner (No. 22-9002, 2023 WL 4482553 (10th Cir. July 12, 2023)).

The IRS’s corporate tax compliance initiatives represent a significant step forward in the agency’s pursuit of fiscal accountability. While the path ahead promises to be challenging, corporations can proactively prepare and protect their interests. The guidance of experienced tax professionals is instrumental in effectively addressing IRS initiatives, preserving corporate rights, and navigating the landscape of corporate tax compliance.

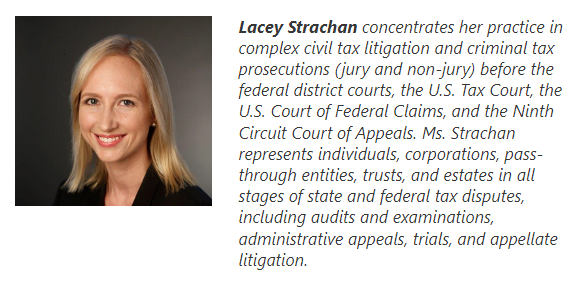

We are pleased to announce that Dennis Perez, Robert Horwitz and Lacey Strachan, will be speaking at the upcoming CalCPA webinar on “Office of Tax Administration: Handling A Case Before California OTA 2023,” October 31, 2023, 9:00 a.m. – 10:00 a.m. (PST).

The OTA (Office of Tax Appeals) has been in operation since January, 2018, but its rules are not well known to many tax practitioners. Learn how to guide a case through the procedural maze of the OTA regulations and avoid foot faults that can jeopardize your client’s case.

Legal Disclaimer. This Report only provides general information about the law and does not, under any circumstances, constitute legal advice in any manner. The facts of each situation are unique and you should not act or refrain from acting in any manner based on any information contained or referenced in this Report at any time without first obtaining the advice of competent professional legal counsel. This site contains links to third-party internet sites. We are not responsible in any manner for, and make no representations or endorsements of any kind whatsoever with respect to, any third-party internet sites or with respect to any information, products or services that such internet sites might offer or provide.