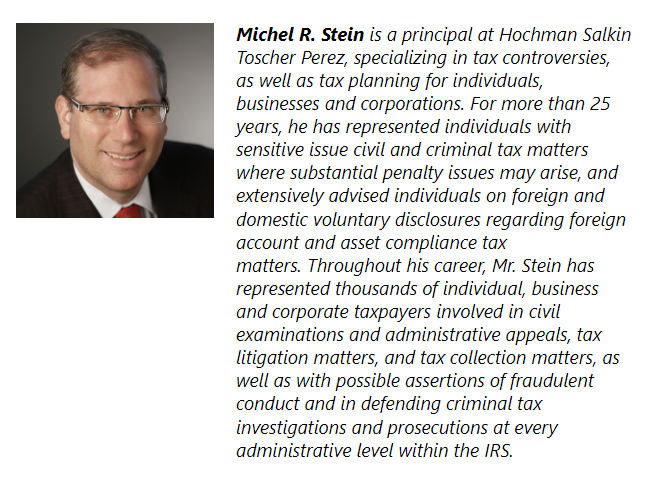

We are pleased to announce that Michel R. Stein will be speaking at the upcoming SVBA webinar “IRS Enforcement Priorities for 2024 and Beyond” Tuesday, June 18, 2024, 12:00 p.m. (PST).

Michel Stein will lead a discussion on what tax practitioners can expect from the Internal Revenue Services’ audit priorities and enforcement action after the Inflation Reduction Act of 2022.

Information about signing up for the webinar can be obtained from the following link:

Not many years ago the government and most practitioners viewed the Anti-Injunction Act as presenting an almost insurmountable barrier to challenges to IRS regulations and rulings. That view began to change with Mayo Foundation for Medical Education & Research v United States, 562 U.S. 44 (2011), which recognized that IRS regulations are subject to review in the same manner as those of any other agency (“we are not inclined to carve out an approach to administrative review good for tax law only”). What this meant for review of IRS rulings and notices became clear in CIC Services, LLC v IRS, 141 S.Ct. 1582 (2021), involving a challenge to IRS Notice 2016-66, which identified certain micro-captive arrangements as listed transactions. The Court held that a person could seek judicial review of an IRS notice to challenge reporting requirements for failure to comply with the Administrative Procedures Act (APA) because to do so was not an attempt to enjoin the assessment or collection of a tax.

Internal Revenue Code §6011(a) authorizes the Secretary of Treasury to issue regulations requiring the filing of returns and statements by “any person.” In 2003, the IRS promulgated Treas. Reg. §1.6011-4, which, for the first time, required taxpayers who participated in “reportable” or “listed” transactions and their material advisors to file reports with the IRS. Treas. Reg. §1.6011-4 (b)(2) defines “listed transaction” as a reportable transaction “determined to be a tax avoidance transaction and identified by notice, regulation, or other form of published guidance as a listed transaction.” In 2004, Congress enacted IRC §6707A, which imposed civil penalties upon taxpayers and material advisors who fail to report listed transactions. For a taxpayer who fails to report a listed transaction these penalties range from $10,000 ($5,000 for a natural person) to $200,000 ($100,000 for a natural person). A material advisor who violates the disclosure provisions faces a penalty of at least $200,000 and up to 50% of the gross income received for its advice or assistance. If a violation is willful, the maximum civil penalty is 75% of gross income and potential criminal charges.

Presently the IRS has identified 36 listed transactions, 28 through notices and the rest through revenue rulings. All of these notices or rulings were issued without notice and comment procedures. There are currently 34 active listed transactions, 28 of which were identified prior to enactment of §6707A. Notice 2017-10 was issued after enactment of §6707A. It “designates certain conservation easement transactions as presumptively tax-avoidant listed transactions.”

On June 4, 2024, the Eleventh Circuit in Green Rock, LLC v. IRS, Case No. 23-11041, affirmed a district court decision invalidating Notice 2017-10 as to Green Rock. The suit was brought by an entity that was a promoter and material advisor of syndicated conservation easements. After issuance of Notice 2017-10 it complied with the filing requirements imposed for listed transactions. Green Rock nonetheless asserted that Notice 2017-20 was invalid because it was not issued in compliance with the notice and comment requirements of the APA.

As the Court noted in its opinion, this past December Congress amended IRC §170(h) to provide that syndicated conservation easements of the type identified in Notice 2017-10 will no longer be allowed to write off easement donations based on inflated valuations.[1] After enactment of this amendment Green Rock ceased syndicating conservation easements.

The Eleventh Circuit began by discussing how, in response to the proliferation of certain corporate tax shelters, the IRS designed the reportable transaction regime to target those shelters and ferret out improper tax avoidance transactions.

An agency ruling that is meant to have the force of law, and violation of which can expose a person to civil or criminal penalties, is a “legislative ruling” and must be issued in accordance with the APA’s notice and comment procedures. The IRS claimed that listed transaction notices were exempt from APA notice and comment procedures. This argument turned on the definition of “reportable transaction” contained in §6707A(c)(1):

“Reportable Transaction-The term “reportable transaction” means any transaction with respect to which information is required to be included with a return or statement because, as determined under regulations prescribed under section 6011, such transaction is of a type the Secretary determines as having a potential for tax avoidance or evasion.”

“Listed transaction” is a reportable transaction “the same as or substantially similar to, a transaction specifically identified by the Secretary as a tax avoidance transaction for purposes of section 6011.” IRC §6707A(c)(2).

As noted by the Court, there is no language in the Code that exempts listed transactions from APA notice-and-comment requirements either expressly or by implication. An agency is exempt from notice and comment procedures only if Congress expressly exempts it. While there is no magical formula for exemption, it will be implied only where Congress has expressly established procedures that are “so clearly different from those required by [the APA] that it must have intended” them to displace the APA procedures.

According to the IRS, the lack of such language was no impediment to finding that the procedure for designating listed transactions was exempt from the APA. Congress had used part of the language of Treas. Reg. §1.6011-(4)(b) in crafting the definitional provisions of §6707A. As a result, Congress was aware of the regulation and must have endorsed the notice procedure for designating listed transactions.

Not so fast, said the Eleventh Circuit. Congressional awareness of the regulation is not enough to overcome the requirements of the APA. That Congress, in drafting §6707A, omitted the “by notice” language contained in the regulation indicates that Congress did not intend to exempt the IRS from notice and comment requirements when designating listed transactions. The Court agreed with the Sixth Circuit in Mann Construction, Inc. v. United States, 27 F. 4th 1138 (2022)[2], that the language of §6707A “cannot bear the weight of the Service’s argument.” In fact, the definition of “reportable transaction”

“can fairly be read to allow the Service to define the substance of a reportable transaction through regulations issued under the Service’s section 6011 authority …. But an indirect series of cross-references hardly suffices to supplant the base-line procedures of the Administrative Procedures Act.”

Congress’ cross-reference was to §6011, which requires the Secretary to prescribe regulations (not notices) for making returns and statements. Congress had the opportunity to adopt the notice procedures when it enacted §6707A but did not. This silence was “the opposite of an express statement.”

Finally, the IRS argued that the Court’s interpretation would invalidate every listed transaction. The Court pointed out that pre-2004 listed transactions were not legislative when issued since they did not result in the imposition of civil or criminal penalties for noncompliance. Section 6707A can be read as ratifying the existing listed transactions without exempting the IRS from prospective notice and comment procedures. In any event, the Eleventh Circuit stated it was only dealing with Notice 2017-10.

Despite prior rulings by the Sixth Circuit and the Tax Court that notice and comment procedures apply to listed transaction designations issued after the enactment of §6707A, IRS has continued to claim that listed transaction notices are exempt. It is unlikely Green Rock will make the IRS change its position. The case, however, further highlights the IRS’s continued vulnerability to challenges for violations of the APA. Practitioners should remain alert to whether IRS guidance which impacts or is contrary to a position of their clients was issued in compliance with APA notice and comment requirements.

_________________________________

[1] A taxpayer can claim a charitable contribution deduction for the donation of a “qualified conservation easement.” Congress added subsection (h)(7) that provides that a contribution by a partnership shall not be treated as a qualified conservation easement “if the amount of such contribution exceeds 2.5 times the sum of each partner’s relevant basis in such partnership.”

[2] In Mann Construction, the Sixth Circuit invalidated Notice 2007-66 for failure to comply with notice and comment requirements.

In 2015 Congress enacted the Bipartisan Budget Act of 2015 (“BBA”) that, among other things, repealed the TEFRA partnership audit provisions and replaced them with BBA partnership audit provisions effective for partnership tax years beginning after December 31, 2017. Both the TEFRA and BBA partnership audit provisions provided for an audit and adjustments at the partnership level. Under the TEFRA provisions any additional tax is assessed against and collected from the individual partners. Under the BBA provisions, however, any “imputed underpayment” is assessed against and collected from the partnership, unless the partnership makes a so-called “push-out election.”

BBA section 1101(g)(4) allowed partnerships to elect into the BBA audit provisions for tax years beginning after November 2, 2015, and before January 1, 2018. To do so, a partnership was required to submit an election that satisfies the requirements of Treas. Reg. sec. 301.9100-22(b)(2). The Tax Court recently addressed the issue of what constitutes a valid election into the BBA audit regime in SN Worthington Holdings, LLC v. Commissioner, 162 T.C. No. 10.

In October 2018, the IRS notified Worthington that its 2016 return had been selected for audit and that it had 30 days within which to elect into the BBA audit procedures. Worthington submitted a completed election form signed under penalties of perjury. One of the representations in the election was that Worthington had sufficient assets to pay and anticipated having sufficient assets to pay the imputed underpayment, as required by Treas. Reg. sec. 301.9100-22(b)(2)(ii)(e)(4). IRS sent Worthington a letter that, based on a review of Worthington’s return it did not have sufficient assets to pay the imputed underpayment and that if it disagreed it should submit documents to the IRS. Worthington did not respond. The IRS subsequently wrote to Worthington that its election was invalid both because it had insufficient assets and that the election was not made by the proper person.[1]

IRS commenced a TEFRA audit of Worthington. In June 2020, Worthington informed the IRS the audit should not be under TEFRA because it had elected into the BBA audit procedures. In August 2020, the IRS issued a TEFRA Final Partnership Administrative Adjustment (FPAA) and Worthington filed a timely petition with the Tax Court. In 2023, Worthington moved to dismiss the case for lack of jurisdiction because the FPAA was invalid. The Court granted the motion.

After reciting the facts, the Court stated that it had jurisdiction over a TEFRA case if (a) there was valid FPAA and (b) a timely petition was filed by the proper person. The IRS argued the election was invalid since the taxpayer was required to provide additional information requested to validate its representations and that allowing an election into the BBA audit procedures when a partnership cannot establish that it has sufficient assets to pay the potential imputed underpayment “would frustrate the purpose of the BBA procedures.” It also argued that based on its failure to respond to the IRS letter and its subsequent actions Worthington should be equitably estopped from arguing that the election was valid.

To decide the motion, the Court had to address two issues: (a) was the FPAA valid and (b) if it was valid, was Worthington equitably estopped from arguing that the FPAA was invalid.

Addressing the first issue, the Court gave a brief overview of TEFRA and BBA audit procedures. Under Treas. Reg. sec. 301.9100-22(a) an election made in accordance with the regulations was valid. The regulations required a written election containing a series of representations, including that the partnership had sufficient assets, and reasonably anticipated having sufficient assets, to pay the imputed underpayment. Since Worthington’s election made this representation, it complied with the regulations.

Discussing valid elections, the Court stated that a taxpayer makes a valid election when it complies “with the plain text of the election requirements.” Once the requirements were met the IRS “may not add ad hoc additional requirements” and “may not require the taxpayer to satisfy more stringent requirements than the provisions authorizing the election.” Since Worthington’s election satisfied the requirement that it had sufficient assets to satisfy an imputed underpayment, the election complied with the regulation.

The Court rejected IRS’s second argument that under Treas. Reg. sec. 301.9100-2(a) an election is invalid if it frustrates the purpose of the BBA and that allowing a partnership to make an election if it did not have sufficient assets to pay the imputed underpayment would frustrate the BBA’s purpose. In addition to pointing to the fact that BBA has procedures where a partnership’s assets were insufficient to promptly pay the imputed underpayment, the Court stated that when there is doubt as to the meaning of a regulation, it is interpreted against the drafter. The IRS could have required partnerships to establish that they had sufficient assets, but it didn’t do so. Since Worthington made a valid election into the BBA audit procedures, the TEFRA procedures were inapplicable and the FPAA issued to Worthington was invalid.

The Court next address whether Worthington was equitably estopped from claiming the FPAA was invalid. To establish equitable estoppel, a party has to show five elements. The first is that there was a false statement or misleading silence by the party claimed to be estopped. Since Worthington never informed the IRS that it made an incorrect determination on the election’s validity for almost two years, there was misleading silence. The second element is that the false representation or misleading silence was about a statement of fact and not an opinion or statement of law. Here, the IRS had all facts needed to determine whether the election was valid. Thus, Worthington’s misleading silence was on a question of law. The third element is that the party claiming estoppel did not know all the facts. Since the IRS had all facts needed to apply the regulation, this element was not established. Thus, the IRS failed to establish two of the five necessary elements for equitable estoppel, and the Court found that equitable estoppel did not apply.

The Court ended by stating that an order of dismissal will be “silenced.”

In making an election, a taxpayer has to make sure that it has complied with all the requirements for the election. These are usually contained in the statute and regulations. If those requirements are met, the Worthington ruling tells us that an IRS challenge to the election cannot be sustained.

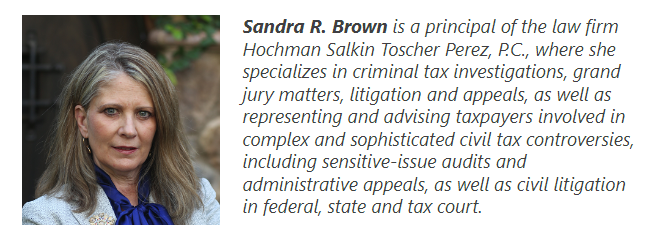

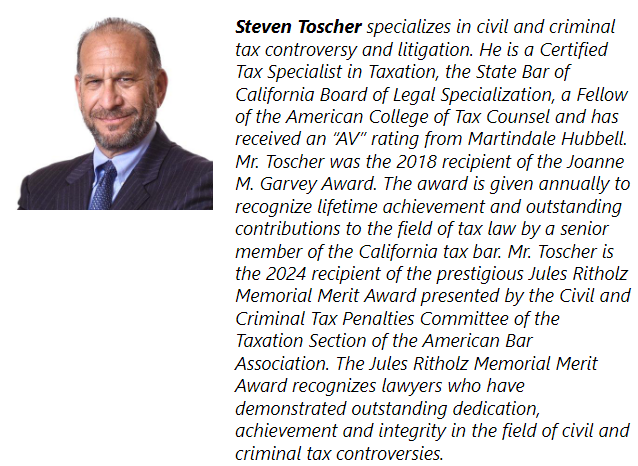

We are pleased to announce that Steven Toscher, Sandra R. Brown and Robert Horwitz will be speaking at the upcoming CalCPA webinar “IRS Scrutiny of ERCs” Tuesday, June 11, 2024, 9:00 a.m. – 10:30 a.m. (PST).

The employee retention credit, enacted as part of the CARES Act, is a US federal tax credit that provides an incentive to employers who continued to employ individuals during the COVID-19 pandemic. Since its enactment, there have been questions as to whether a business qualified and how to interpret what qualified as a full or partial suspension of operations in order to be eligible for the credit. Companies engaged advisors – some of whom were diligent in determining a businesses’ eligibility – though others engaged advisors, whose business models created incentives to take aggressive positions on employee retention credit qualification that likely are not sustainable under audit. This panel will discuss the IRS’ increased enforcement efforts in the area of Employee Retention Credits (ERC), explain how to spot red flags indicating abuse of the ERC, describe the civil and criminal penalties that can apply to taxpayers, promoters and practitioners for erroneously claiming ERC credits, and provide tips on how to help clients correct mistakes where appropriate.

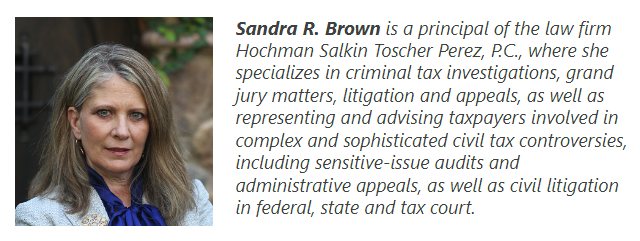

We are pleased to announce thatSandra R. Brown will be receiving the prestigiousRichard Carpenter Excellence in Tax Award from the USD School of Law – RJS LAW Tax Controversy Institute. The Award is being presented at the 9th Annual USD School of Law – RJS LAW Tax Institute taking place July 19th in San Diego, California.

This award is given to an individual who exemplifies honesty, integrity, ethics, and compassion throughout their careers in the field of tax controversy and has demonstrated outstanding dedication and expertise while representing taxpayers before the federal and state governments.

Sandrais a principal of the law firm Hochman Salkin Toscher Perez P.C., where she specializes in criminal tax investigations, grand jury matters, litigation and appeals, as well as representing and advising taxpayers involved in complex and sophisticated civil tax controversies, including sensitive-issue audits and administrative appeals, as well as civil litigation in federal, state and tax court.

Prior to entering private practice, Ms. Brown served as the Acting United States Attorney, First Assistant United States Attorney, and Chief of the Tax Division in the Office of the U.S. Attorney, Central District of California. During her 27 years as a trial lawyer, she personally handled over 2,000 tax cases on behalf of the United States before the United States District Court, the Ninth Circuit Court of Appeals, the United States Bankruptcy Court, the United States Bankruptcy Appellate Panel, and the California Superior Court. Included in those cases are two U.S. Supreme Court decisions and a multitude of published 9th Circuit decisions.

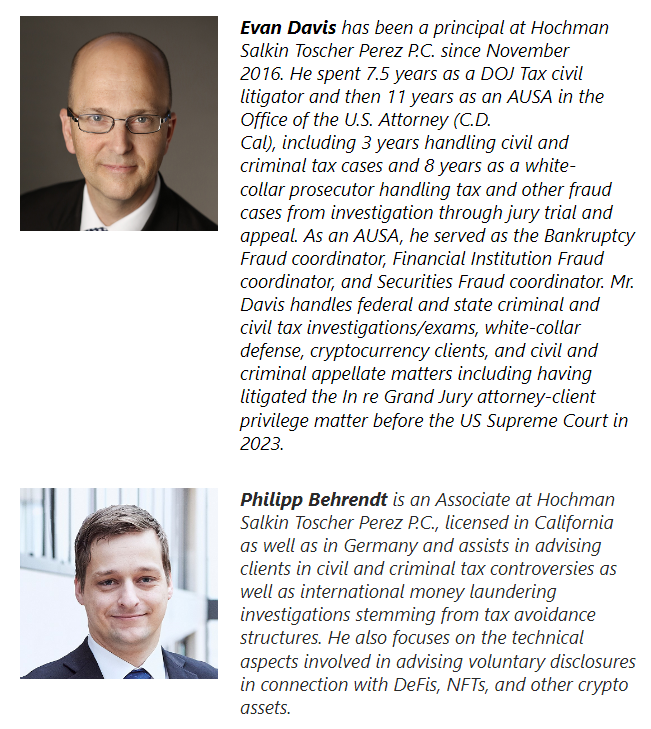

We are pleased to announce that Michel R. Stein and Philipp Behrendt will be speaking at the upcoming CSTC San Francisco Chapter webinar on “Cryptocurrency Tax Compliance: Tax Filing Requirements, Managing IRS Examinations & Tax Treatment of Digital Currency,” on Wednesday, June 5, 2024 from 6:00 p.m. – 8:00 p.m. (PST).

Cryptocurrency has exploded over the last few years causing significant concerns regarding the taxation of these transactions for sellers, purchasers, and investors. Tax counsel and accountants representing clients holding and selling cryptocurrency, including those engaging in mining, exchanges, staking and lending, must understand applicable tax rules and reporting requirements for these transactions. During the webinar we will discuss: The various types of cryptocurrency and exchanges, valuation issues, tax reporting requirements for cryptocurrency exchanges, disclosure requirements for cryptocurrency ownership, tax treatment of hard forks, staking and lending transactions and the likelihood of criminal investigations and prosecutions for failing to properly report cryptocurrency transactions, and the use of the IRS Voluntary Disclosure policy to get into compliance including “qualified amended returns” to avoid penalties.

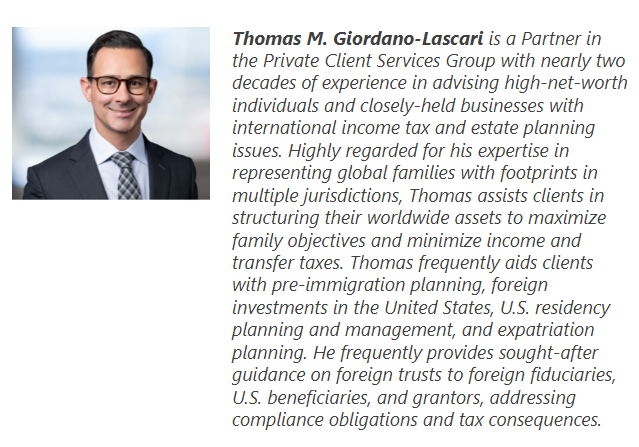

We are pleased to announce that Steven Toscher, Michel R. Stein and Thomas M. Giordano-Lascari (Greenberg Glusker)will be speaking at the upcoming Strafford webinar “IRS Audits of Expatriates: Section 965 Transition Tax, Exit Tax, Non-Filers, and the Examination Process“ Tuesday, May 28, 2024, 10:00 a.m. – 11:30 a.m. (PST).

The IRS has and continues to audit a higher proportion of ex-pat tax returns. The rules for these nonresidents are often the reverse of those for residents. The filing status Married Filing Jointly can require a special election. Self-employed taxpayers usually are not entitled to deduct expenses. A simple presence in the U.S. for 183 days can trigger capital gains. Remarkably, two-thirds of expats file these complicated returns on paper.

The IRS continues its compliance campaign focusing on Section 965 transition tax payments. The Service required these payments by U.S. shareholders of certain foreign corporations on unrepatriated (untaxed) earnings as part of the 2017 Tax Act. The IRS stated that these audits could be expanded to other issues, particularly those relative to the 2017 Tax Act.

Tax professionals and advisers working with individuals who have relocated abroad must understand the issues triggering these IRS audits, prepare clients for these audits, and know how to handle these demanding examinations.

Listen as our panel of foreign tax experts discusses reporting requirements of expatriates’ issues for non-filers, guides tax practitioners through the examination process, and explains best practices to withstand the ongoing scrutiny of these taxpayers’ returns.

Sandra R. Brown was quoted in a May 6, 2024 Tax Notes Article on What the IRS’s 2024 ‘Dirty Dozen’ List Tells Us About Tax Administration, authored by Kathy A. Enstrom, Moore Tax Law Group, LLC.

The IRS annually releases its “Dirty Dozen” list to warn taxpayers and tax practitioner alike of various tax scams as well abusive transactions that the Service will be focused on in the coming year. While many topics on the annual list are “repeat offenders”, there is always something new to be aware of. One might say that, akin to the anticipation of learning who will be drafted in the first round of the annual draft for your favorite professional sport, tax professionals as well as non-tax professionals look forward each year to the IRS’s release of its “Dirty Dozen” list. As noted by Sandra ….

“. . .The value of what can fairly be described as an IRS ‘tradition’ in releasing the ‘Dirty Dozen’ couldn’t be any clearer than a simple internet search,”

“You’ll get almost a million hits in less than .34 seconds showing that beyond the expected accounting firms and tax professionals, there are banks, credit unions, insurance advisers, universities, software companies, state taxing authorities, news publications, and the list goes on, of those posting the IRS’s Dirty Dozen list.”

For an in-depth review of what the Dirty Dozen list tells us about tax administration, what types of scams the IRS is advising taxpayers to be on the alert and diligent in protecting themselves and their personal financial information as well as tax avoidance strategies that the IRS has been challenging and will continue to scrutinize, please check out Kathy’s article, visit https://www.irs.gov/newsroom/dirty-dozen, or contact an experience tax professional.

In a recent interview with CNBC at the Chainalysis Links event in New York, Guy Ficco, a Chief of the IRS Criminal Investigation Division (IRS-CI), issued a stark warning: the IRS is gearing up to tackle a significant increase in cases of tax fraud and evasion related to cryptocurrency transactions.

Ficco’s words carry weight, especially in the ever-evolving landscape of cryptocurrency tax regulation and enforcement. He emphasized that the IRS has observed a noticeable surge in what he termed “pure crypto tax crimes” (so-called Title 26 cases) and is no longer only part of non-tax scams such as fraud and embezzling. Ficco anticipates this trend to continue in the foreseeable future. These Title 26 crimes encompass a range of activities, from failing to report income generated from crypto sales to deliberately concealing the true basis of cryptocurrency holdings.

“This could be purely not reporting income generated from crypto sales, it could be hiding the true basis of crypto, or shielding the true basis in crypto. So, that is an area where we’ve seen an uptick and I anticipate we’re going to see more of and there is going to be more charged title 26 crypto cases here, in this year and going forward.” Guy Ficco (Chief of IRS CI)

The implications are clear: the IRS is not only focused on the growing prevalence of crypto-related tax offenses but is also taking proactive measures to address them head-on. Ficco also underlines that the agency has forged public private partnerships with leading blockchain analysis firms like Chainalysis, along with other law enforcement agencies. These collaborations aim to enhance the IRS’s capabilities in tracing and identifying illicit financial activities within the cryptocurrency ecosystem.

Ficco highlighted the expertise of IRS special agents in tracking financial transactions while at the same time acknowledging the unique challenges posed by the decentralized and pseudonymous nature of cryptocurrencies. To bridge this gap, the IRS is leveraging the specialized tools and knowledge offered by firms like Chainalysis, which are instrumental in the IRS’s unraveling complex crypto transactions and uncovering illicit activities.

What does this mean for crypto investors and enthusiasts? Firstly, it underscores the importance of complying with tax obligations related to cryptocurrency transactions. The IRS is ramping up its efforts to detect and prosecute individuals who flout tax laws, whether through ignorance or deliberate evasion. Ignoring these obligations could lead to severe penalties, including fines, penalties, and even criminal charges.

Moreover, the IRS’s heightened scrutiny serves as a reminder of the evolving regulatory landscape surrounding cryptocurrencies. As governments around the world grapple with how to regulate this burgeoning asset class, individuals and businesses operating in the crypto space must stay informed and adapt to changing compliance requirements. This includes maintaining accurate records of crypto transactions, reporting income from crypto-related activities, and seeking professional guidance when necessary.

For those who may have previously neglected their tax obligations related to cryptocurrency, Ficco’s statements serve as an important wake-up call. The IRS is not only actively pursuing current violations but also casting a retrospective eye on past non-compliance. Individuals who have failed to report crypto income or provided inaccurate information on their tax returns may find themselves facing increased scrutiny and potential legal consequences.

In conclusion, Ficco’s remarks paint a clear picture: the IRS is bracing for a surge in crypto tax crimes and is prepared to take decisive action to enforce tax compliance within the cryptocurrency ecosystem. As the regulatory landscape continues to evolve, it’s imperative for crypto investors and enthusiasts to stay informed, comply with tax obligations, and seek professional guidance to navigate this complex terrain. Failure to do so could result in serious repercussions, both financial and legal.

This is a fierce warning to taxpayer that the time of leniency is over and erroneous tax reporting will be criminally charged. We recently blogged on the first purely tax related crypto charges in the case against a Texas man.

Our firm specializes in advising clients on proactive measures to mitigate criminal exposure while also providing expert representation in criminal cases.

Employing many of the same tools as the IRS, such as Chainalysis, blockchain explorer and others, to assist in not only staying abreast but ahead of the information available to the IRS, so that we can effectively advocate for our clients’ interests and address any challenges that may arise in the process.

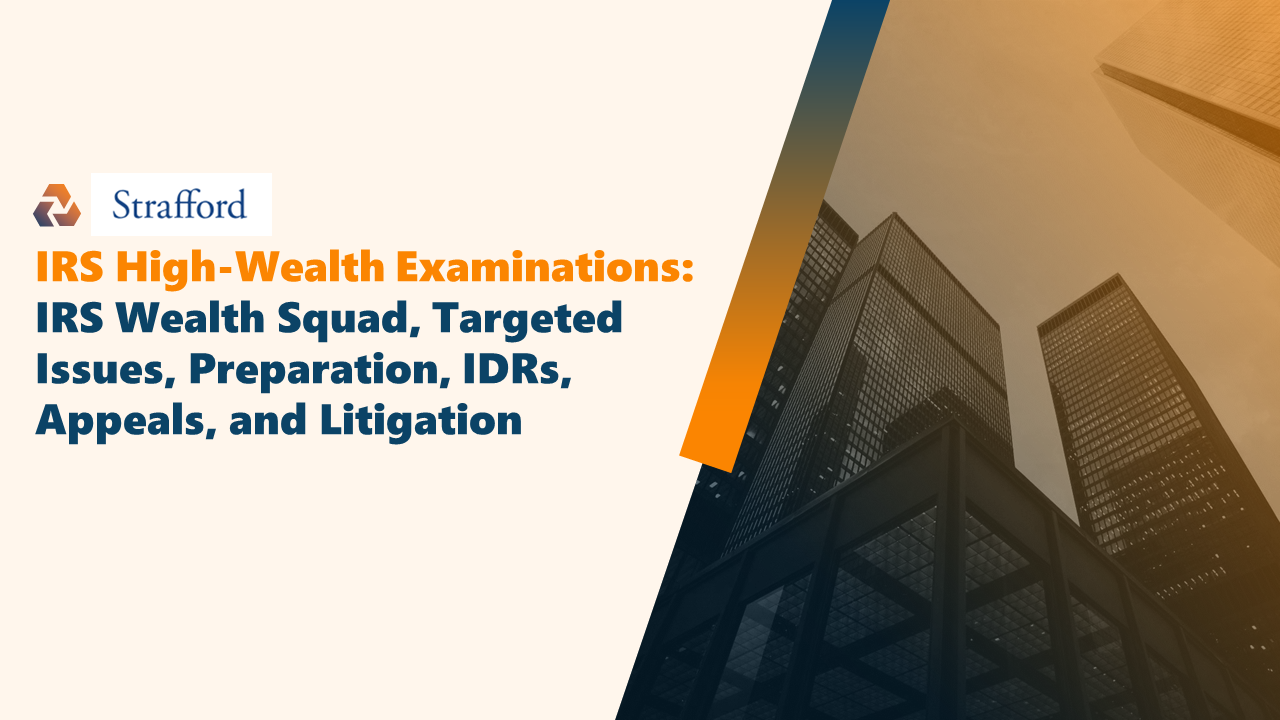

We are pleased to announce that Steven Toscher, Michel R. Stein and Cory Stigile will be speaking at the upcoming Strafford webinar “IRS High-Wealth Examinations: IRS Wealth Squad, Targeted Issues, Preparation, IDRs, Appeals, and Litigation” Wednesday, May 15, 2024, 10:00 a.m. – 11:50 a.m. (PST).

The IRS Large Business and International Division is auditing high net worth individuals and their related entities, including partnerships, S corporations, trusts, and private foundations. The Wealth Squad, a highly-trained division of the IRS, is conducting these audits.

These examinations will target recently enacted and complex areas of taxation, including:

Section 199A Qualified Business Income Deduction

Section 163(j) Business Interest Deduction Limitation

Section 965 Repatriation of Previously Untaxed Foreign Earnings

Section 172 Net Operating Loss Deduction Refund Claims

Required foreign reporting of trusts, bank accounts, assets, etc.

Although targeting specific areas, these are comprehensive audits covering most aspects of a taxpayer’s tax return. Tax professionals working with high-wealth clients need to prepare for potential examinations and understand how to represent these taxpayers.

Legal Disclaimer. This Report only provides general information about the law and does not, under any circumstances, constitute legal advice in any manner. The facts of each situation are unique and you should not act or refrain from acting in any manner based on any information contained or referenced in this Report at any time without first obtaining the advice of competent professional legal counsel. This site contains links to third-party internet sites. We are not responsible in any manner for, and make no representations or endorsements of any kind whatsoever with respect to, any third-party internet sites or with respect to any information, products or services that such internet sites might offer or provide.