We are pleased to announce that Michel R. Stein, Evan Davis and Philipp Behrendt will be speaking at the upcoming CalCPA Cryptocurrency Compliance webinar, Tuesday, August 13, 2024, 9:00 a.m. – 10:30 a.m. (PST).

The program will provide tax advisers and compliance professionals with a practical look at IRS guidance for calculating and reporting income and gain on cryptocurrency (e.g., Bitcoin) transactions. We’ll discuss the IRS’s latest positions on cryptocurrency, analyze IRS efforts to increase compliance and define proper reporting and the tax treatment for convertible virtual currency and cryptocurrency, stablecoins, as well as NFTs. We will address recently released Broker Reporting Regulations, the latest released IRS Guidance, the recent IRS enforcement initiatives to identify digital asset activity, how the IRS enforcement strategy fits into the voluntary disclosure practice, and the risks of criminal prosecution related to unreported and improperly reported cryptocurrency transactions.

Click Here for More Information

For more information, please contact Michel R. Stein at stein@taxlitigator.com

For more information, please contact Evan Davis at davis@taxlitigator.com

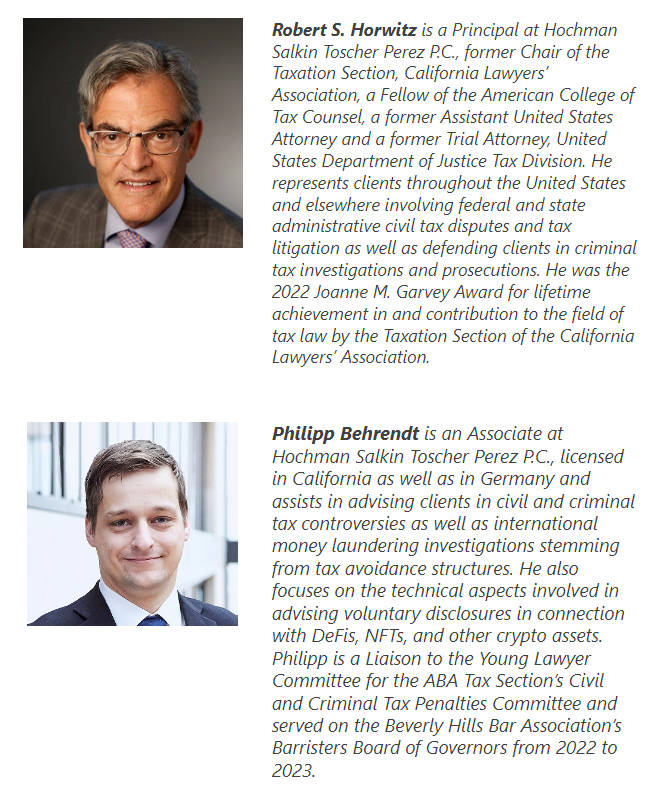

For more information please contact Philipp Behrendt at behrendt@taxlitigator.com